Canada’s heavy-duty aftermarket grew in 2023, but headwinds remain

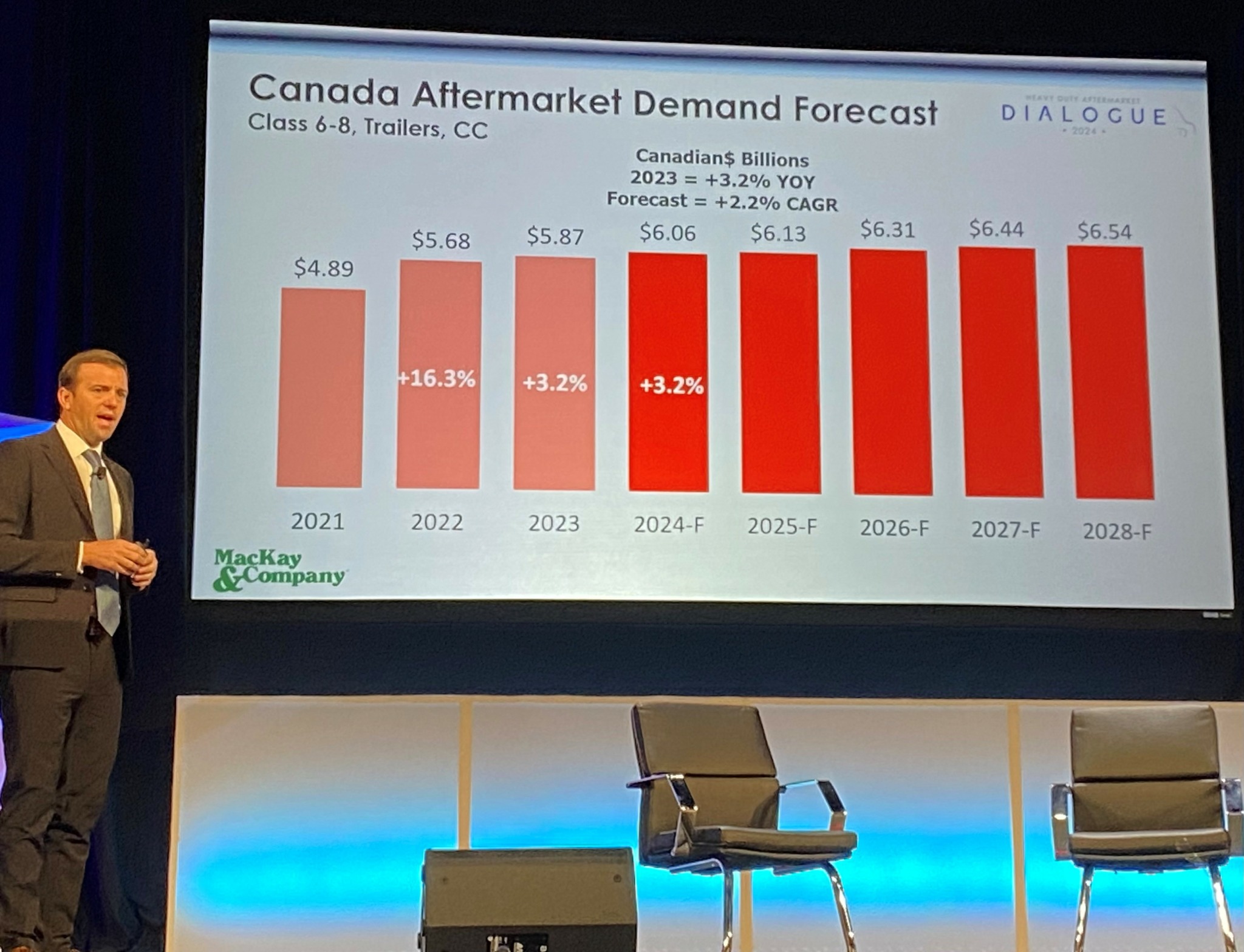

The total value of Canada’s heavy-duty parts aftermarket, including Classes 6-8 trucks, trailers, and container chassis, increased 3.2% last year to CDN$5.87 billion.

And MacKay & Company anticipates it will grow by the same amount this year, bringing its value to $6.06 billion. Travis Kokenes, research manager for MacKay & Company, updated attendees on the state of the aftermarket at Heavy-Duty Aftermarket Dialogue in Dallas, Texas, this week.

Canadian Class 8 retail sales, at 30,00 units, were up 3% in 2023, while trailer sales rose 2% to 42,000 units and Classes 6/7 retail sales totaled 9,000 sales, up 13%. Canada now has 375,000 Class 8 trucks on the road, but will shed 0.4% of its size to 373,000 units by 2028, MacKay & Company suggests.

The trailer population will edge down 0.1% from 582,000 units to 581,000 over the same time, reflecting a stagnant heavy-duty equipment population. (Canada is the only one of the three countries, including the U.S. and Mexico, that will see a decrease in total vehicle populations, MacKay & Company predicts).

Classes 6-8 truck utilization came in at 84.6% for the year, according to the analyst, and surveyed fleets anticipate it will decrease another 1% in the first quarter, and 1.5% in Q2. MacKay itself anticipates utilization to hold at 84.5% in Q1, and 85% in Q2. Trailer utilization, meanwhile, ended the year at 88.7% with fleets anticipating a Q1 drop to 86.2% and MacKay taking a more optimistic view of 87.5%.

Parts prices stabilizing

Fortunately for fleets, parts pricing is beginning to normalize. After a 10.2% increase in 2022 and 6.7% increase in 2021 – both years well above the historic 30-year average – parts prices in 2023 rose just 3.9% and are anticipated to rise 3% this year, still above the long-term average.

And, Kokenes added, “parts shortage problems, while they still exist, tended to peak back in May 2022, where prices peaked in September of that year. They have been moderating ever since.”

MacKay & Company surveyed fleets and distributors on their biggest concerns. Fleets ranked them, in order: price increases, parts availability, and government/regulations. Distributors listed their top concerns as: price increases, labor issues, and parts availability.

The lack of parts has been particularly troublesome for distributors. More than half reported they lost a sale due to the fact they didn’t have the part a customer needed in a timely manner. The value of those lost sales ranged from US$500 to $100,000, averaging $28,950.

“Things have improved, but they’re not nearly where we want them to be quite yet,” Kokenes said of the parts shortages.

Asked what dealers and distributors can do to improve things, surveyed fleets said: have parts available by improving inventory (36%); freeze price increases (34%); and improve overall customer service (10%).

Macro-economic outlook

Bob Dieli, economist with MacKay & Company, warned broader macro-economic conditions could create further headwinds for the heavy-duty aftermarket. He explained we’re in the “boom phase” of the current cycle, but “as long as the Fed is in a bad mood, we’ve got problems.”

Showing a graph displaying five key metrics – total truckable economic activity (TEA), consumption, investment, exports, imports and government spending – all were red except government, which was flashing yellow.

“We don’t see any upside in the major components of TEA,” Dieli said.

Eyes turn to the U.S. Fed to see where the economy will go, and Dieli said the real precursor to recession is when it pivots and begins lowering interest rates.

“Every recession has the Fed’s palm prints on its back,” he said, noting a pivot appears to be several months away.

Dieli said a soft landing “is possible, but not probable.” And he left attendees with three crucial questions to ask themselves in these uncertain conditions: How is my biggest customer doing? How is my biggest supplier doing? And, how are my biggest competitors doing?

“The best outlook I can give you now for 2024 is for limited upside on the part of TEA,” he concluded.

Have your say

This is a moderated forum. Comments will no longer be published unless they are accompanied by a first and last name and a verifiable email address. (Today's Trucking will not publish or share the email address.) Profane language and content deemed to be libelous, racist, or threatening in nature will not be published under any circumstances.