ECONOMIC TRUCKING TRENDS: Industry sentiment improving and spot market flatbed rates continue to rip

ACT Research recently held a two-day seminar and reports fleets are feeling “cautiously optimistic” about the year ahead, while remaining cautious about ordering new equipment.

They want to first make sure the improving market conditions are “for real,” ACT reports.

They feel real for flatdeckers, having seen spot market pricing improvements in 13 of the past 14 weeks. Van and reefer rates slid last week, but that’s normal for that particular week. The important thing is, they remain resilient and stronger than in past years over the comparable period.

Industry sentiment improving: ACT Research

Industry forecaster ACT Research recently held a two-day commercial vehicle outlook seminar and reports that attendees expressed ‘cautious optimism’ for 2026.

Attendees on an OEM panel indicated that customers are feeling better about the industry’s prospects this year but are not rushing to order equipment as they wait for further signals that the improvement is for real.

“There is still an excess of equipment in the market, and carrier profitability is still down, so that means less capex spent on equipment. Expectations are that it will take at least a quarter or two before fleet profitability flips and equipment buying picks up,” ACT Research said in a roundup.

ACT’s Tim Denoyer gave a market and forecast update.

“The for-hire freight cycle is getting ready to turn,” he said. “Capacity contraction should drive demand. Tighter capacity plus the longest downturn this century equals a shift from late cycle to early cycle.”

On the Class 8 market, analyst Carter Vieth cautioned that: “Despite the recent spot rate surge, carrier profitability remains weak. Fleets still lack capex but expect improvement in 2026.”

But, he added, “The Class 8 forecast has increased on the better-than-expected economy heading into 2026, surge in spot rates, EPA27 clarity, and the surge in December orders.”

“Trailer customers have skipped buying cycles,” added ACT’s Jennifer McNealy, “but remain hesitant and concerned about pricing. Fleets are balancing capex between power and trailing equipment ahead of EPA27. OEMs are navigating subpar demand at the start of 2026 with continued uncertainty while looking for opportunities.”

Trailer market headwinds continue to blow

In its latest State of the Industry: U.S. Trailers report, ACT Research noted the near-term future remains challenging for trailer suppliers.

“Cancellations gyrated between earth and outer space through most of 2025, before returning to a more subdued rate, 1.8% as a percentage of backlog, in December. The new year opened with a still elevated but more stable 1.6% rate in January,” said McNealy. “Data continued to show elevated cancellations in the dry van and tank segments.”

“For a second consecutive month, net orders significantly outpaced build, pumping some life into the anemic backlogs on the books through most of 2025. Backlogs rose more than 18% sequentially, or about 12k units, ending January at 75,500 units.”

She noted challenges including weak demand/order activity, financing concerns, tariffs (both known and unknown), weak freight volumes and carrier profits all seem poised to remain.

“However, the uptick in net orders the past two months has built the backlog queue and given industry leaders reason to believe that 2026 could be the year of transition that everyone has been hoping to have,” McNealy added.

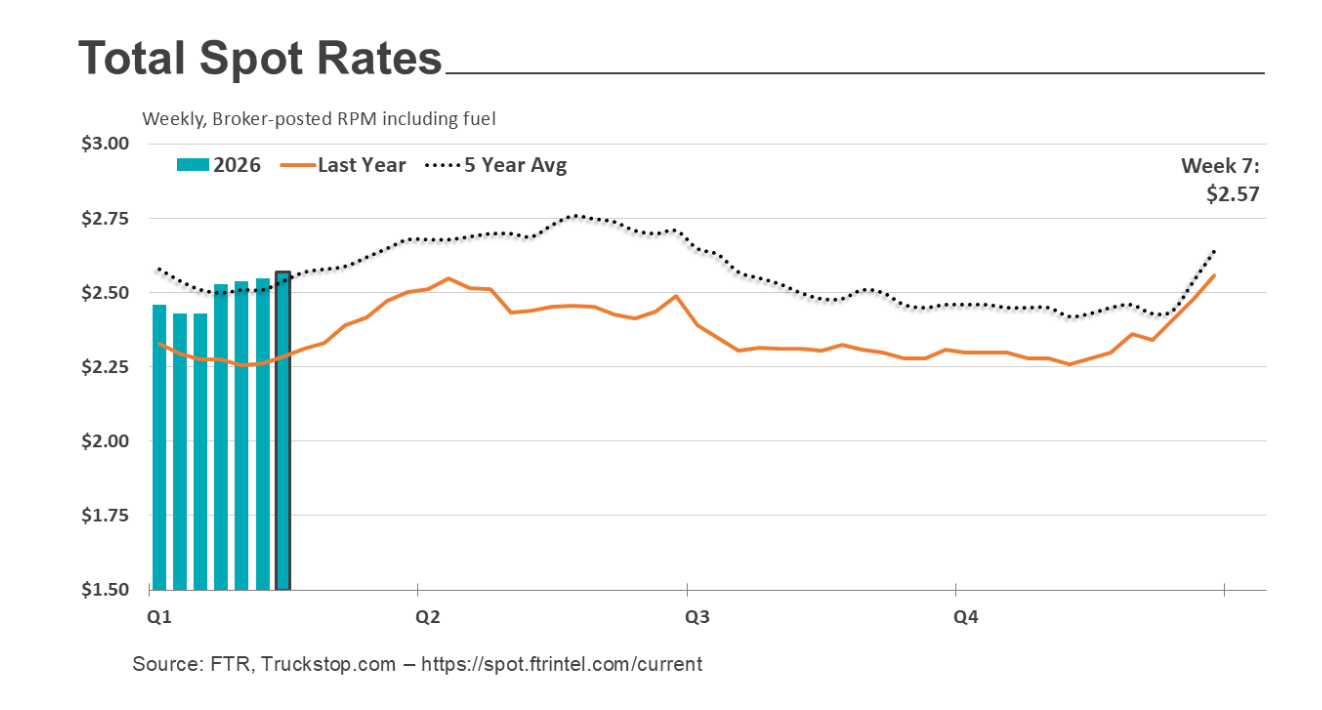

Spot market continues to firm up

U.S. spot market prices remained strong during the week ended Feb. 20, according to the latest data from Truckstop.com and FTR.

While rates declined sequentially for dry van and reefer equipment, rates remained strong compared to the same weeks between 2023 and 2025. Flatbed rates are ripping, having risen in 13 of the past 14 weeks, and are now at their strongest levels since the spring of 2022.

“In most years, van equipment rates would still be normalizing after holiday stress, so the decreases since the big winter weather impact in late January are in line with seasonal expectations,” Truckstop.com reported. “That normalization typically begins to taper off in late February, and the latest winter storm in the northeastern U.S. could provide additional near-term support for dry van and refrigerated rates this week and into March.”

Total load postings increased only modestly, but they reached a milestone, the highest level since July 2022. Coupled with a slight decrease in truck postings, the volume gain produced a Market Demand Index of 145.0, which is the second-highest level since March 2022.

Have your say

This is a moderated forum. Comments will no longer be published unless they are accompanied by a first and last name and a verifiable email address. (Today's Trucking will not publish or share the email address.) Profane language and content deemed to be libelous, racist, or threatening in nature will not be published under any circumstances.