ECONOMIC TRUCKING TRENDS: Spot rates surge, Class 8 orders dip but remain ‘exceptionally strong’

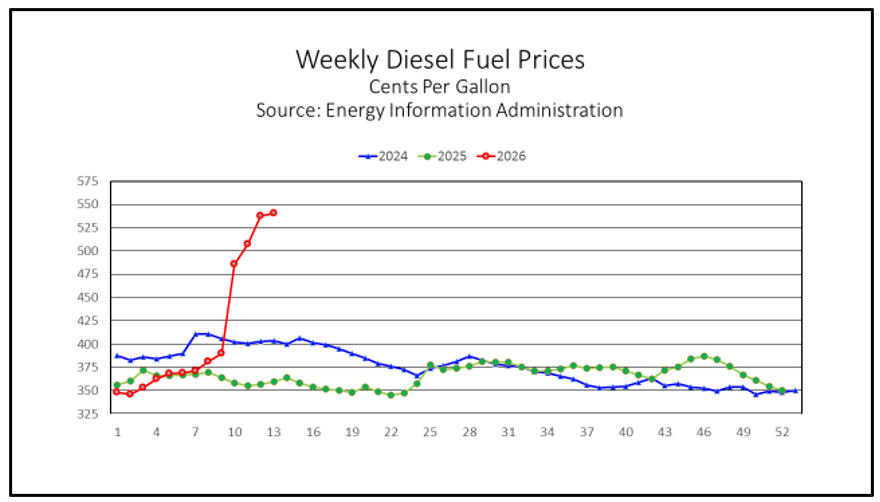

What’s rising faster, the cost of diesel or spot market rates? Both are increasing rapidly. And Class 8 orders pulled back in March from a record February but remained “exceptionally strong” according to FTR.

Meanwhile, the Middle East conflict and rising diesel prices are reshaping fleet economics, according to a new report from CMVC.

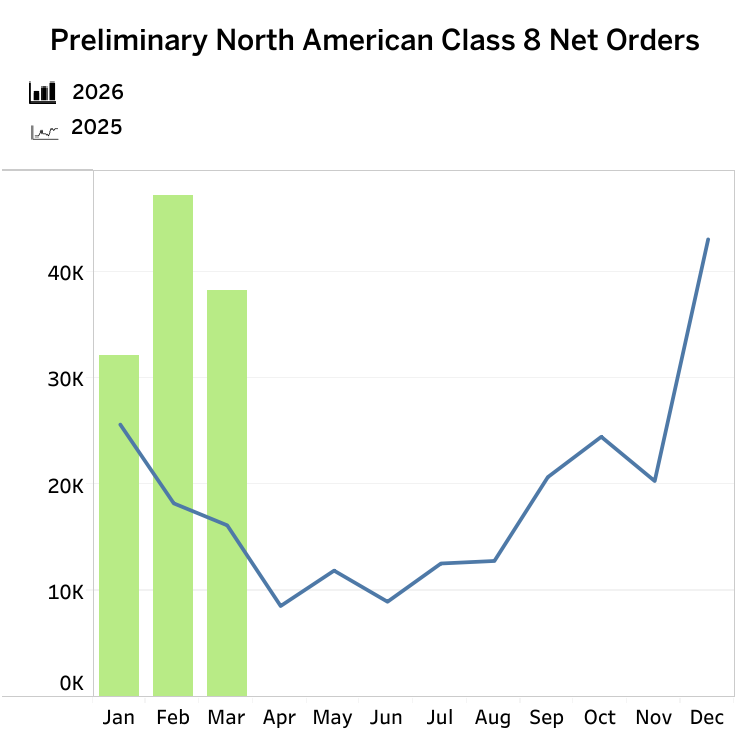

Class 8 orders pull back in March, but remain strong

Preliminary data point to Class 8 orders of 38,200 units in March, an “exceptionally strong” number according to FTR, while still falling 19% from February’s tally.

March numbers were up 137% year over year, marking the fourth consecutive month of greater than 20% year-over-year growth.

“The 2026 order season from September 2025 through March 2026 is now up 15% year over year, representing a clear inflection from the double-digit declines seen earlier in the cycle and reinforcing the view that the industry has entered the early stages of recovery,” said Dan Moyer, senior analyst, commercial vehicles with FTR.

“While monthly variability is likely to persist, improving cumulative order trends and a strengthening freight backdrop suggest demand is becoming more durable and less reliant on short-term catch-up dynamics. At the same time, disciplined OEM production continues to support backlog growth without leading to excess inventory.”

Moyer said risks remain, including the trajectory of the freight recovery, high financing costs, policy uncertainty and geopolitical factors influencing fuel prices.

“In addition, several new risks are introduced by the surge in orders itself. First, there is potential for a FOMO effect in which fleets rush to place Class 8 orders to secure build slots, thus introducing some excess into backlogs and raising the risk of higher cancellation rates later in the year, especially if the freight recovery slows or falters,” Moyer added.

“Second, if current order strength proves fundamentally driven, it raises the question of whether the industry can successfully ramp production to these elevated levels given potential supply chain and labor constraints.”

FTR notes the surge in order activity reflects replacement demand, rather than new capacity entering the market.

For its part, ACT Research reported 37,200 orders.

“After one of the best Class 8 order numbers in history in February, it is little surprise March preliminary data retreated, but only slightly, to a still very strong 37,200 units,” said Carter Vieth, research analyst at ACT Research. “Though, as we exit ‘order season’ (September to March), and in recognition of significant backlog building since December, order strength is likely to move off current levels on typical seasonality. The Iran war poses major risks to the economic outlook, but tight for-hire capacity and a return of the driver shortage have helped insulate spot rates from the negative impacts of rising diesel prices.”

Fuel shock, driver squeeze reshape fleet economics: CMVC

Fleets are facing a rapidly shifting operating environment as geopolitical tensions drive up fuel costs and tighten capacity, with impacts likely to persist, according to CMVC.

A conflict involving Iran, the U.S. and Israel has disrupted energy flows through the Strait of Hormuz, triggering a spike in global energy prices and pushing up diesel costs. The disruption has also constrained supplies of commodities such as aluminum, fertilizers and chemicals, adding to broader inflationary pressure.

CMVC said fleets are absorbing higher fuel bills now, but the bigger impact will come as elevated energy prices filter through the economy, weighing on freight demand.

At the same time, a tightening supply of CDL drivers — compounded by the closure of more than 3,000 truck driving schools and limits on non-domiciled CDLs — is expected to push wages higher.

Rising fuel, labor and equipment costs are squeezing margins. While tighter capacity could support higher freight rates, any gains may be offset by wage pressures.

Further cost increases are coming with the EPA’s 2027 emissions standards, which are expected to raise truck prices and could prompt some fleets to pull forward purchases into 2026.

CMVC warned the broader economy could drift toward stagflation, with fleets focused in the near term on cutting costs, improving productivity and passing along higher expenses where possible.

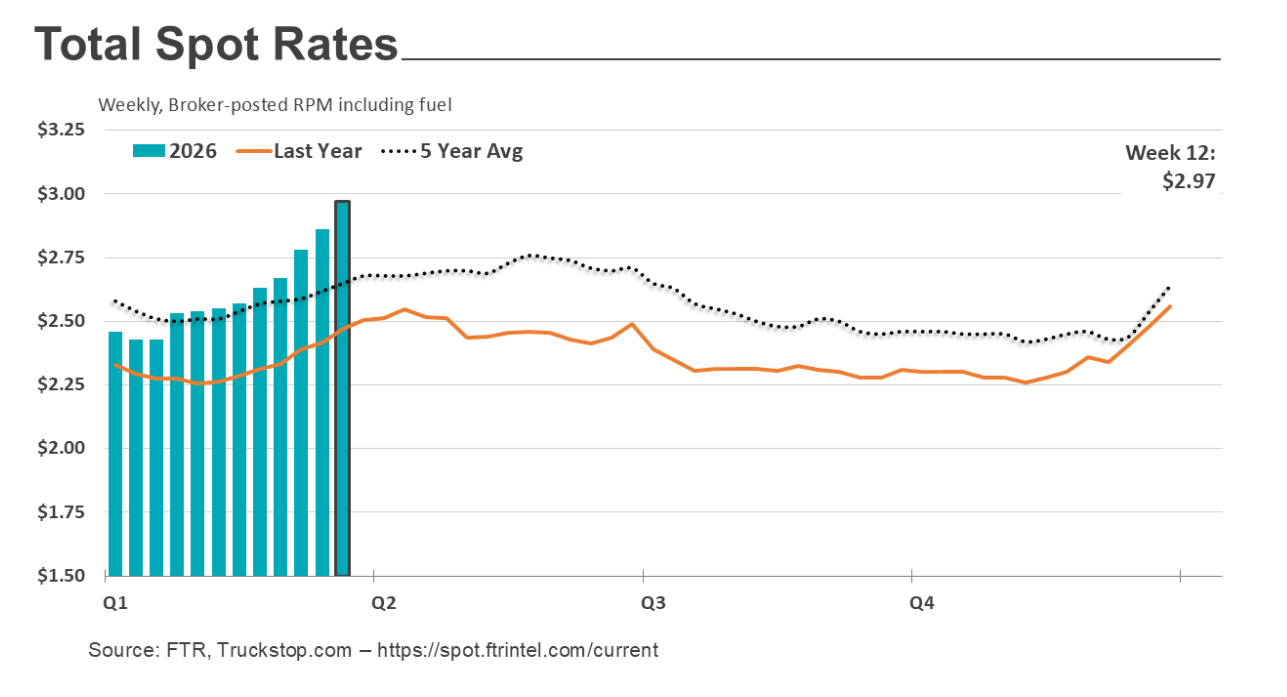

Spot market rates rise again

Spot market rates rose sharply for the week ended March 27, but record high diesel prices are likely to eat into those gains.

Flatbed rates saw one of their largest increases on record, according to Truckstop.com, and are now at their strongest level seen since August 2022. Dry van rates are now at their highest levels since June 2022 and reefer rates are their best since the end of 2022 (excluding a couple anomalies due to severe weather).

“Dry van and refrigerated spot rates are very strong compared with the same 2025 period, even when excluding the portion of rates required for carriers to recover escalating fuel costs. Flatbed rates are not as strong year over year, but that is primarily because of unusually strong rates during the same period last year,” Truckstop.com reported.

Total load postings rose to their highest level since June 2022. With only a small increase in truck postings, the Market Demand Index rose to 178.1, the highest level since February 2022.

Have your say

This is a moderated forum. Comments will no longer be published unless they are accompanied by a first and last name and a verifiable email address. (Today's Trucking will not publish or share the email address.) Profane language and content deemed to be libelous, racist, or threatening in nature will not be published under any circumstances.