Economic Trucking Trends: Latest data sends mixed signals on industry health

This week’s trucking-related economic data painted a convoluted picture for the industry. For-hire truck tonnage took a healthy jump, but remained in freight recession territory. Overall trucking conditions improved, but remained weak.

New carrier registrations in the U.S. are down, while exits are still elevated. And we have a new State of Logistics report from Penske to digest. Let’s dive in.

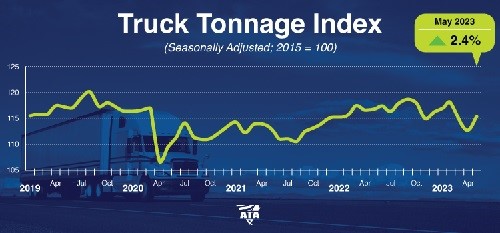

Truck tonnage jumps

U.S. for-hire truck tonnage spiked 2.4% in May, according to the latest data from the American Trucking Associations (ATA), but it wasn’t enough to shake off the freight recession.

“Tonnage had a nice gain in May, but remains in recession territory,” ATA chief economist Bob Costello said in a release. “The 2.4% gain didn’t erase the 4.5% total drop the previous two months. Additionally, tonnage continues to contract from year earlier levels as retail sales remain soft, manufacturing production continues to fall from a year ago, and housing starts contract from 2022 levels.”

Year over year (YoY), tonnage was down 1.3% in May – the third straight YoY decrease.

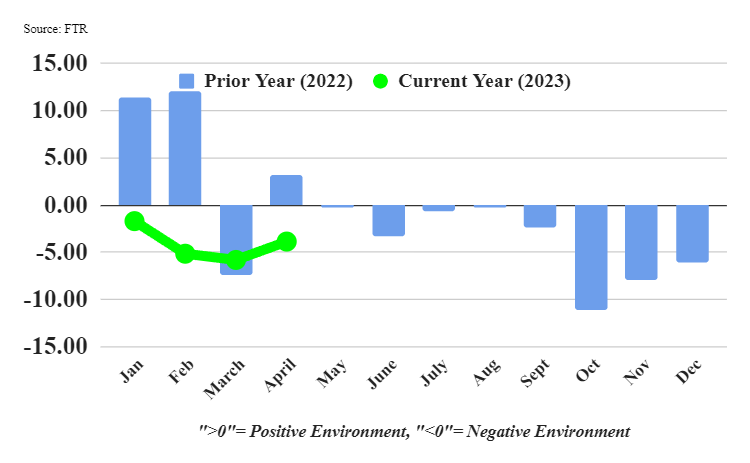

Trucking conditions improved, but remain weak

While still in negative territory, trucking conditions as measured by industry forecaster FTR’s Trucking Conditions Index (TCI) improved in April to a reading of -3.88. That was a two-point jump from March readings thanks to stronger freight volumes and a “somewhat less negative environment” for financing costs.

Weaker capacity utilization and slowing fuel costs decreases weighed on the index, which is expected to remain in negative territory through mid-2024, FTR reports.

“Our estimates and forecasts still show the truck freight market at close to its bottom, but the outlook remains quite weak,” said Avery Vise, FTR’s vice-president – trucking. “For example, we see almost no improvement in capacity utilization into 2024, which would keep freight rates soft. Some upside potential exists for better market conditions, including a stronger automotive sector and a deeper loss of driver capacity than we are forecasting currently, but trucking companies should not count on those developments. Freight demand might remain just strong enough to limit the number of drivers exiting the market, thereby keeping utilization weak.”

Carriers’ appetite for new trailers decreasing

Getting build slots for new trucks, and especially trailers, is getting easier, according to ACT Research. This is especially true for trailers where cancellations are escalating. While ACT said “the sky isn’t falling” for trailer makers, it also noted “more ominous clouds on the horizon.”

In its State of the Industry: U.S. Trailers report, ACT Research reported higher cancellation rates and lower backlogs for trailer manufacturers.

“While the broad-based nature of cancellations suggests the turn is starting to come into focus, this is juxtaposed against a backdrop of rather robust backlogs, even with declining orders,” said Jennifer McNealy, director – commercial vehicle market research and publications at ACT Research.

Regarding cancellations, McNealy added, “Fleet commitments remained mixed in May. Total cancels grew to 4.2% of backlog, higher than April’s 2.8% and significantly higher than March’s 0.9% rate. That said, while several segments were at or below 1.5%, dry vans rose to 4.1%, reefers are now at 6.5%, and flatbeds hit 4.7%. April’s increase raised an eyebrow, but we cautioned that one month does not a trend make. With two consecutive (and large) jumps in cancellations, both eyes are now wide open.”

She concluded, “Some trailer makers are telling us customers are cutting back on their anticipated order appetite for this year and next, and that fewer customers are on the sidelines to pick up whatever equipment/build slots become available. Clearly, the demand dynamic is shifting.”

On the power unit side, heavy- and medium-duty retail sales are up double digits so far this year. Backlogs are being chewed through as production has increased thanks to improving supply chains.

“Heavy-duty and medium-duty production were essentially in line with build plans. May’s Class 8 build rate was a healthy 1,343 units per day, representing the ninth month in the past 12 where build rate exceeded 1,300 units per day,” reported Eric Crawford, ACT’s vice-president and senior analyst.

“We expect positive momentum to slow in [the second half of] 2023. More so in Q4. Already, one of the critical components of heavy vehicle demand, carrier profitability, is increasingly under pressure. In Q1, the public carriers’ profits declined to levels last seen in early 2020. While some of the decline was seasonal, public TL carrier margins were down 250 basis points year over year. With contract rates expected to deteriorate into Q4, profit margins should continue to narrow.”

State of Logistics: The Great Reset

The 2023 CSCMP State of Logistics Report, authored by Penske, was released this week and paints a picture of a supply chain reset. Last year’s report centered around “out of sync” supply chains still recovering from Covid-related disruptions.

“While the pandemic is still not fully behind us — and may be with us in some form or another for

several years to come — it is no longer closing shops or congesting seaports,” the report indicates.

This year the supply chain is being brought back into sync and is about “resetting relationships, assumptions, and practices for a world transforming.”

Supply chain managers, the report says, are focused less on transactions and more on strategic and holistic approaches to their function’s role.

The report, which is available for download, noted motor carriers saw little change in overall volume last year, while capacity increased putting pressure on rates.

“These changing dynamics have induced shippers — who turned toward dedicated fleets to address the capacity challenges arising during the peak months of the pandemic — to seek a new balance among dedicated, private, and one-way services,” the report concludes. “Carrier margins were threatened by low rates and high resource costs, with smaller carriers – reliant on the spot market – under particularly acute pressure.”

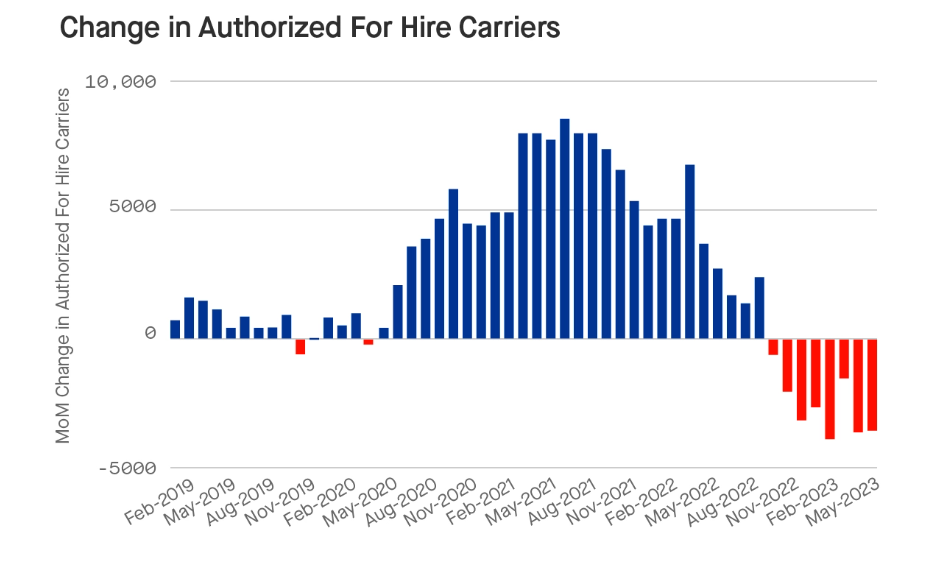

Fewer new carrier registrations, more exits

Motive put out its June economic report this week, which showed no reprieve from the freight recession, but indicated new carrier registrations dipped to their lowest levels since June 2020. This, while carrier exits maintained elevated April levels.

“The slowing of carrier exits expected in Q2 has not yet materialized, as May saw 3,500 carriers exit the market, similar to levels seen in April,” Motive reported.

“Meanwhile, there were less than 7,200 new carrier registrations last month. This represents a 22% month-over-month decrease that matches levels last seen in June of 2020, before the pandemic freight explosion.”

Have your say

This is a moderated forum. Comments will no longer be published unless they are accompanied by a first and last name and a verifiable email address. (Today's Trucking will not publish or share the email address.) Profane language and content deemed to be libelous, racist, or threatening in nature will not be published under any circumstances.