ECONOMIC TRUCKING TRENDS: Class 8 build slots near capacity as van spot rates hit record high

Fleets are running out of time to secure Class 8 build slots in 2026, ahead of EPA27 emissions regulations that are expected to push up the cost of new trucks in January.

And while some may be getting their orders in ahead of that price hike, others may be seeking new equipment to take advantage of a strong U.S. spot market.

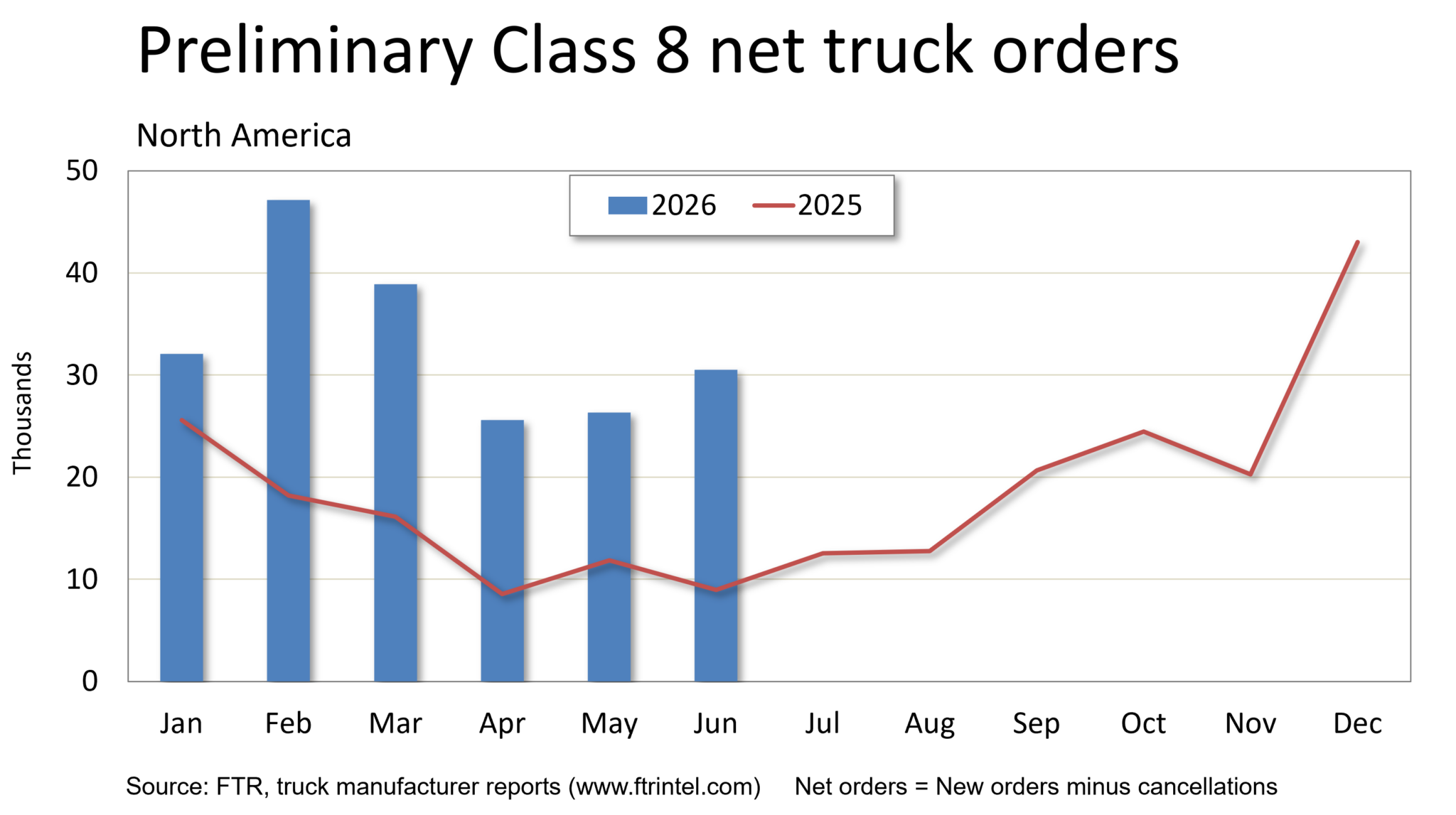

Class 8 truck orders remain red hot as 2026 build slots near capacity

North American Class 8 truck orders remained exceptionally strong in June, with preliminary data from both ACT Research and FTR showing fleets continue placing orders despite dwindling 2026 production availability.

ACT Research pegged preliminary June Class 8 net orders at 31,400 units, up 231% from a year earlier, while FTR estimated 30,500 units, a 16% increase from May and 241% above June 2025.

The strong showing extends a seven-month streak of robust order activity, driven by improving freight market conditions.

“Truckers only buy trucks when they make money,” said Carter Vieth, research analyst at ACT Research. “Underscoring the rapid change in carrier fortunes, freight rates continue to soar.”

FTR said June represented the second-largest June order total since it began tracking the market. Orders are now running 36% ahead of last year’s order season, with remaining 2026 production slots expected to fill this month if they haven’t already.

That could push new orders into early 2027 production, shifting attention to pending changes to the U.S. EPA27 nitrogen oxide emissions rules and how aggressively the agency enforces the new standards.

“June orders confirm that the Class 8 cycle remains constructive, as monthly intake continues to surprise to the upside,” said Dan Moyer, senior analyst of commercial vehicles at FTR. “The bigger question now is not demand but how much of the 2026 backlog converts to production before uncertainty over EPA, tariffs, and USMCA reshapes fleet timing for 2027.”

ACT also reported preliminary Classes 5-7 orders totaled 20,700 units in June, up 67% year over year. While a resilient U.S. economy continues to support demand, Vieth said dealer inventory stocking ahead of the 2027 emissions regulations likely accounted for much of the increase.

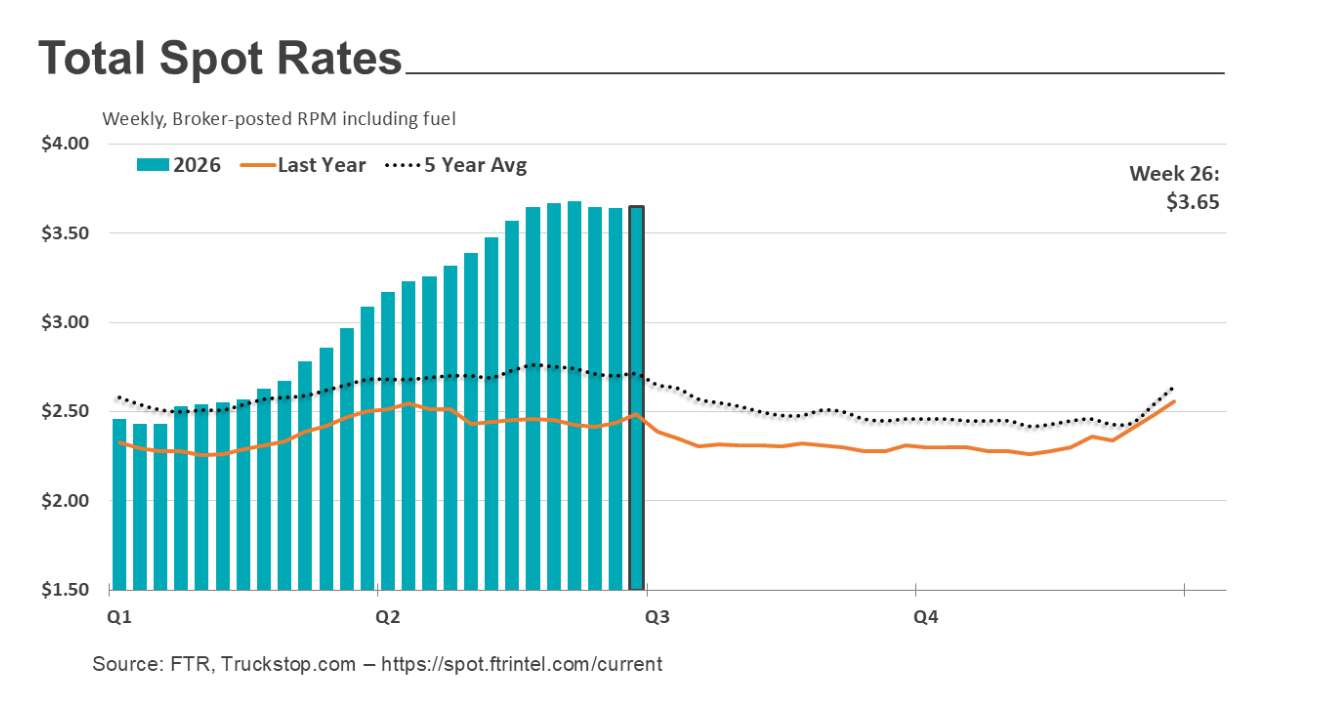

Dry van spot rates hit record high ahead of July 4 holiday

Spot market demand cooled during the week ending July 3 as freight volumes eased following the June shipping rush, but dry van rates climbed to a record high in what is traditionally one of the strongest pricing weeks of the year.

According to Truckstop and FTR Transportation Intelligence, the overall Market Demand Index (MDI) fell 46.4 points to 132.6 as available loads declined 26.9% week over week, while truck postings slipped just 1.3%. Despite the weekly decline, the MDI remained 87.1% higher than the same week last year.

The national average spot rate across all equipment increased 0.2% to $3.65 per mile, while the national average diesel price fell 15 cents to $4.70 per gallon.

Dry van rates posted the strongest gains, jumping 3.8% to a record $3.10 per mile. FTR said the week leading into the July 4 holiday has historically produced some of the largest seasonal increases in van pricing. The dry van MDI fell 59.8 points to 286.3 as load postings declined 19.8% and truck availability dropped 3.1%.

Refrigerated freight also saw strong pricing, with spot rates climbing 7.1% to $3.71 per mile, the fourth-highest level on record. Reefer load availability declined 8.6%, while truck postings increased 12%, pushing the segment’s MDI down 62.6 points to 278.8.

Flatbed rates slipped for a third consecutive week, falling 0.3% to $3.82 per mile, although FTR noted pricing remains within a few cents of record levels. Flatbed load postings fell 33.3%, while truck availability declined 2.9%, resulting in a 76.4-point drop in the segment’s MDI to 167.5.

The specialized market also weakened, with rates falling 1.2% to $3.62 per mile. Load availability declined 23.5% and truck postings edged down 0.5%, reducing the specialized MDI to 29.5.

Despite softer demand following the holiday, spot rates remain well above year-ago levels across all equipment types, with dry van, reefer and flatbed rates each up roughly 50% compared to the same week in 2025.

Have your say

This is a moderated forum. Comments will no longer be published unless they are accompanied by a first and last name and a verifiable email address. (Today's Trucking will not publish or share the email address.) Profane language and content deemed to be libelous, racist, or threatening in nature will not be published under any circumstances.