Economic Trucking Trends: Class 8 orders remain strong, dry van rates lead spot market gains

The latest Class 8 orders suggest fleets are still confidently placing orders despite weak freight conditions and overcapacity in the market, with ACT Research characterizing the truck market as “solid, rather than stellar.”

U.S. spot market rates and volumes bucked seasonsal trends post-U.S. Thanksgiving, with dry van haulers seeing the largest rate gains. And freight brokers saw a stronger than expected third quarter.

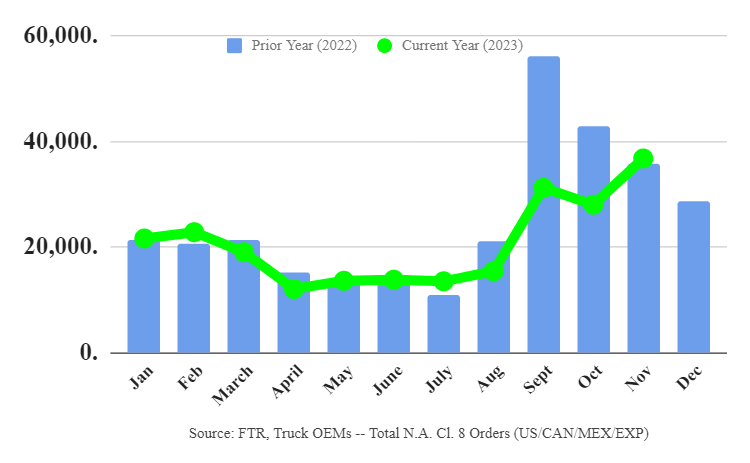

Class 8 orders strengthen

Class 8 truck orders jumped 32% in November to 36,750 units, FTR reports in preliminary data, but the gain was just 2% on a year-over-year basis. Build slots continue to be filled “at a healthy rate,” according to the industry forecaster, reflecting “a market that is still performing at a high level historically.”

“We also saw a more cohesive market for OEMs versus October with the majority seeing increases in orders,” summed up FTR chairman Eric Starks. “Despite prolonged weakness in the overall freight market, fleets continue to be willing to order new equipment. Order levels were above the historical average but continue to follow seasonal trends, stabilizing our expectations for replacement demand in 2024.”

Forecasting rival ACT Research reported 41,700 orders on the month.

“November Class 8 net orders were the highest monthly intake since October 2022,” said Kenny Vieth, ACT’s president and senior analyst. “A modest seasonal factor presses down gently this month, with seasonal adjustment dropping November’s seasonally adjusted intake to 40,100 units, making November the best ‘real’ order month since September 2022.”

He added, “Even though backlogs, in seasonal fashion, are rising, they continue to point to a different market vibe heading into 2024: Still good, for sure, but solid rather than stellar.”

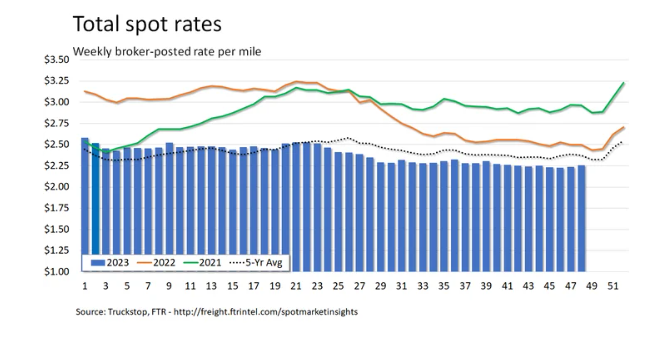

Spot market rewarding dry van haulers

The U.S. spot market was led upward by dry van rates for the week that ended Dec. 1, according to Truckstop and FTR Transportation Intelligence. Broker-posted dry van rates were up more than 17 cents/mile over the past two weeks, reaching their highest level since February.

Each equipment segment saw rates increase from the prior week, but gains paled in comparison to dry van numbers. Total rates were “modestly higher” during the week in which rates typically fall following U.S. Thanksgiving.

Load postings on the Truckstop network more than doubled for the week after the holiday, to levels not seen since September. Truck postings didn’t keep up, driving the Market Demand Index (MDI) to 62.5, its highest level since May. The dry van MDI was the strongest so far this year.

3PLs seeing improving freight conditions

The Transportation Intermediaries Association (TIA) put out its 3PL Market Report, Third Quarter 2023, highlighting a stronger freight economy than expected. It’s keeping expectations in check, however, due to sluggish freight volumes and trucking overcapacity, which will likely keep conditions soft until the second half of 2024, the association says.

“Our forward-looking data has had us bracing for continued weakness in the freight economy,” said TIA president and CEO Anne Reinke. “However, the surprising strength we saw during the third quarter goes to show that the market can still outperform forecasts. Our members continue to be incredibly resilient and have made the most of less-than-stellar conditions in recent quarters.”

The freight economy, or GDP Goods Transport Sector, rose 6.5% from the previous quarter, ending a five-quarter streak of negative or nearly negative quarter-over-quarter growth. TIA members saw quarter-over-quarter declines in shipments (-2.2%) and total revenue (-0.2%) but a 2.1% increase in the invoice amount per shipment.

“We’re looking at tough year-over-year comparisons for brokers given that the third quarter of 2022 was a strong one for members,” said Mark Christos, TIA chairman and chairman of the Market Report. “That being said, the positive results detailed in this most recent report are encouraging for members as we brace for further headwinds until mid-2024.”

By segment, intermodal and LTL saw quarter-over-quarter gains in total shipments, while truckload shipments slipped.

Further takeaways

Additional observations from the TIA’s latest report:

- Trucking capacity has not declined enough to tighten the market

- Consumer spending remains strong, but could be undermined by job growth weakness

- The manufacturing sector was boosted by motor vehicles and parts output

- Strong output during Q1 and Q2 could’ve been related to a production increase ahead of the UAW strikes. It’s uncertain whether output will resume at pre-strike levels or return to weaker levels.

Have your say

This is a moderated forum. Comments will no longer be published unless they are accompanied by a first and last name and a verifiable email address. (Today's Trucking will not publish or share the email address.) Profane language and content deemed to be libelous, racist, or threatening in nature will not be published under any circumstances.