Economic Trucking Trends: Reefer rates improve on spot market, October trailer orders rise

What are truck and trailer orders telling us about overall freight conditions? ACT Research has noted a few trends: vocational demand is driving Class 8 orders, and trailer demand has been decent the last couple months but cancellations remain elevated.

The latest week was unexciting on the spot market, but reefer rates saw a seasonal improvement.

Trailer orders start new order season strong

Preliminary net trailer orders from ACT Research totaled 35,300 units in October, down 26% year over year, but up nominally from September numbers.

“Preliminary net orders, at 26,200 seasonally adjusted, were about 9% lower sequentially,” said Jennifer McNealy, director commercial vehicle market research and publications at ACT Research. “While this certainly continues the positive momentum for the industry that began last month, two months of robust orders does not guarantee the full year. It’s still early in the new year order season to call.”

Cancellations remain elevated, ACT reported, primarily in the platform and tank segments. Some specialty segments are sold out until late 2024.

Class 8 orders powered by vocational demand

Meanwhile, Class 8 orders were down 24% year over year in October but orders were strong relative to freight market conditions.

“Final Class 8 net orders were 32,287 units in October, with the largest drivers of orders being market segments with lingering pent-up demand,” said Kenny Vieth, ACT’s president and senior analyst. He’s referring to vocational trucks, which saw orders surge 24%. We recently heard from Mack Truck executives that the segment is getting a boost from infrastructure spending related to the U.S. Inflation Reduction Act.

Class 8 tractor orders, on the other hand, were down 34% year over year. Build rates were below expectations, retail sales ticked down resulting in an increase in inventory, ACT reported.

“For carriers, the long bottom in freight rates continues, with spot rates little changed since April,” Vieth said. “A big driver of rate weakness has been lagged private fleet capacity additions. As for-hire fleets tend to be the first buyers in line, private fleets have been the drivers of Class 8 market strength in 2023, adding equipment at the bottom of the cycle and prolonging the rate pain.”

Van trailer demand forecast trimmed

Taking a holistic look at Class 8 truck and trailer demand, ACT has pulled back forecasts for dry van demand due to a recalibration of its expectations regarding power-only brokerage.

“To accomplish the scheme of introducing drop-and-hook productivity into the small carrier spot market was a plan by large fleets and brokerages to boost trailer-to-tractor ratios, build trailer pools, etc., into the wildly growing pandemic stimulus and supply-chain constrained spot market,” said Vieth. “From Q1 2021 to Q2 2022, DAT’s spot market postings averaged nearly 4.9 million loads per day. Year to date, DAT’s spot posts have averaged less than 1.4 million loads per day, a 71% decline from the heady average experienced at the peak of the pandemic freight bubble.”

The sharp rise and fall in spot market activity reflects a lot of freight getting to where it was originally intended to go, but couldn’t due to capacity limitations in private fleets and other dedicated operations. Pulling back on this heretofore anticipated ratio expansion lowers the trajectory of the dry van market.

Vieth concluded, “One of the things staying our hand from deeper forecast cuts, in the face of weak freight fundamentals, has been a solid industry-wide start to ‘order season.’ The last trimester of the year is the period in which the OEMs usually open their out-year order books, leading to a period of outsized orders that typically extends into March.”

ACT Research believes that “it’s different this time” factors are at work in 2024, and those factors will help support Class 8 demand around fundamentally weak U.S. and Canadian tractor markets.

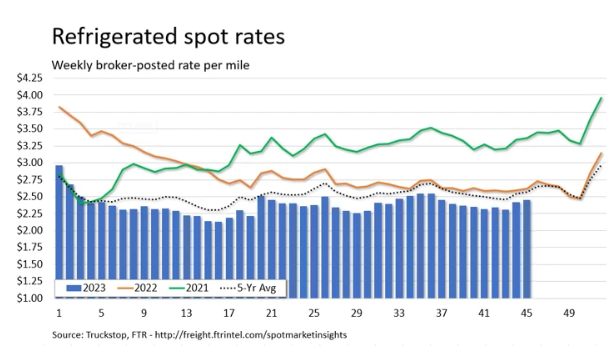

Reefer rates lead

Truckstop and FTR Transportation Intelligence report the week ended Nov. 10 showed a U.S. spot market that moved in line with seasonal expectations, though both rates and volume are below year-ago levels.

Reefer rates saw a second consecutive week of gains, the first time that’s happened since early September. Dry van rates were flat and flatbed rates had their worse decline in five weeks. Things could get better for dry van rates, as their holiday-period strength tends to lag reefer by a couple weeks, Truckstop reported.

Truck postings were flat, so with a decline in overall load postings, the Market Demand Index slid to 49.7.

Have your say

This is a moderated forum. Comments will no longer be published unless they are accompanied by a first and last name and a verifiable email address. (Today's Trucking will not publish or share the email address.) Profane language and content deemed to be libelous, racist, or threatening in nature will not be published under any circumstances.