Spot market tightens as fuel costs, Roadcheck and cross-border demand push rates higher

North America’s spot freight market continued to show signs of tightening through April and into May, driven by higher fuel costs, stronger outbound Canadian freight demand and a sharp disruption tied to International Roadcheck enforcement week.

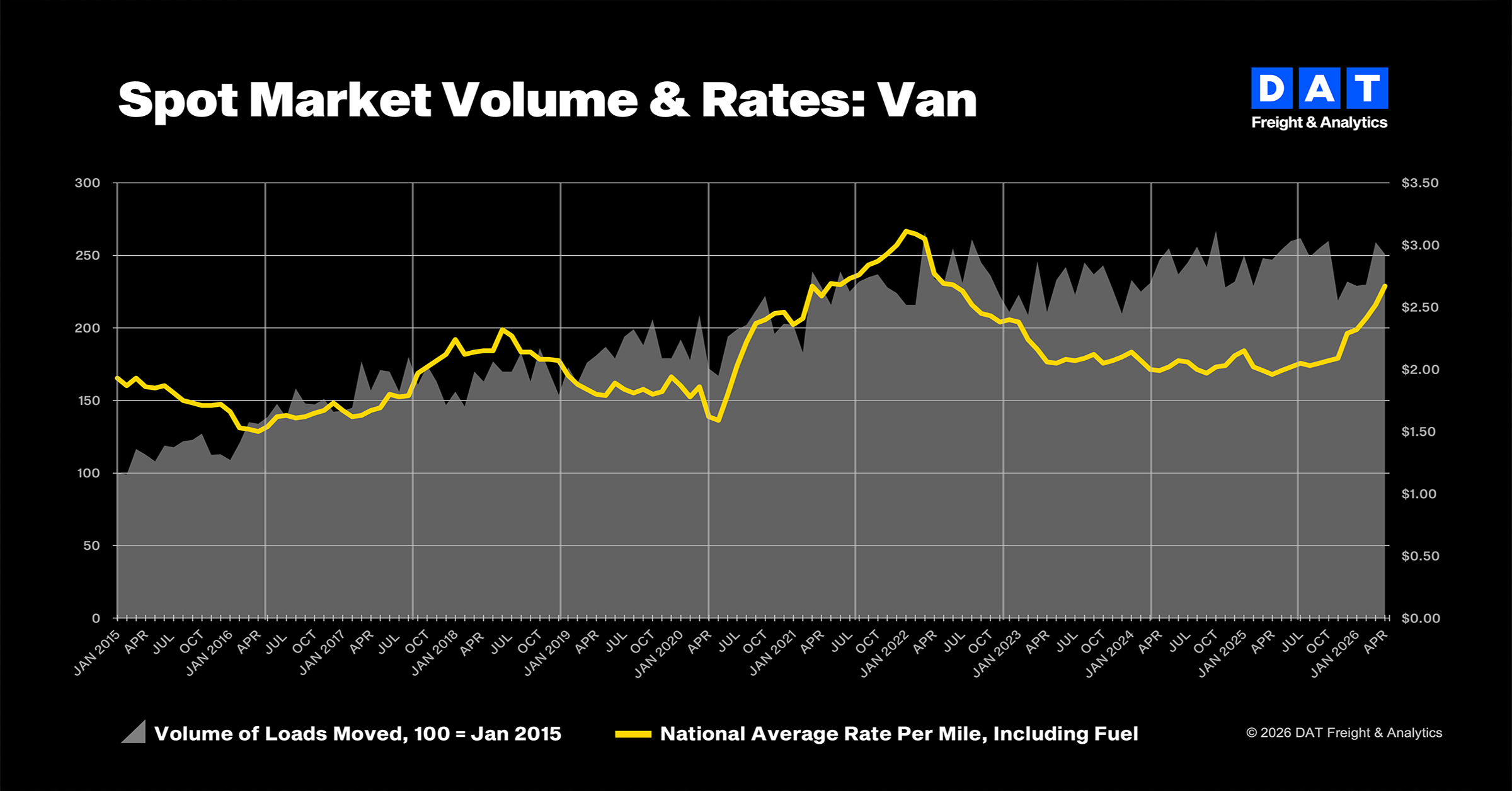

DAT Freight & Analytics reported truckload spot and contract rates climbed sharply in April, although much of the increase was tied to fuel surcharges rather than stronger underlying freight demand.

At the same time, Canada’s spot market saw unusually strong outbound cross-border demand, while truckstop.com reported a surge in spot activity and rates during International Roadcheck week as carriers temporarily pulled trucks off the road.

“Fuel was the story in April,” said Dean Croke, principal industry analyst at DAT. “Linehaul rates barely moved in van and reefer, and the volume of loads moved fell across the board. Small carriers continue to exit the market under sustained cost pressure. That’s not what a demand-based truckload freight recovery looks like.”

DAT said April freight volumes declined month over month across all major equipment categories. Its Truckload Volume Index showed van volumes fell 3% from March, reefer volumes dropped 9%, and flatbed freight slipped 3%.

Despite softer freight volumes, spot rates rose sharply due largely to higher diesel costs. National average spot van rates climbed to $2.67 per mile in April, up 15 cents from March and 71 cents higher than a year earlier. Reefer rates rose to $3.11 per mile, while flatbed rates jumped to $3.46 per mile.

However, DAT noted that linehaul rates excluding fuel showed only modest gains in van and reefer freight, suggesting demand remains uneven.

Flatbed freight showed the strongest signs of actual tightening, with linehaul rates increasing 25 cents per mile in April.

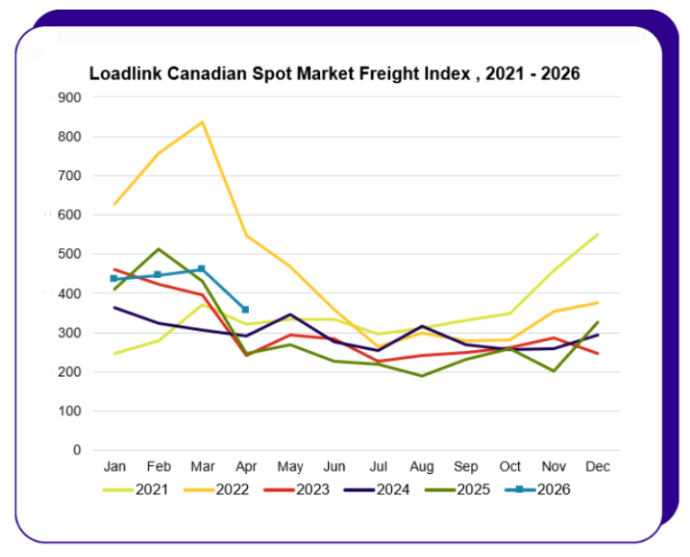

In Canada, Loadlink reported freight volumes eased from March levels but remained significantly stronger than a year ago, particularly on southbound cross-border lanes.

Outbound loads from Canada to the U.S. were up 122% year over year in April, the strongest annual gain Loadlink said it has seen in recent memory.

Overall, Canadian spot freight volumes declined 23% from March, following a strong first quarter, but still finished 44% above April 2025 levels.

Loadlink said outbound cross-border freight accounted for the largest share of Canadian postings and continues to outpace inbound freight growth, giving carriers stronger leverage on southbound lanes.

“Every spring has its rhythm, and April typically settles after a busy Q1,” said James Reyes, general manager at Loadlink. “What stands out this year is the strength of outbound freight; it’s running at a pace we haven’t seen in some time, and that changes how carriers approach southbound negotiations.”

Capacity loosened somewhat during April, with the truck-to-load ratio rising to 1.86 trucks per load from 1.28 in March. However, the ratio remained 35% lower than April 2025, indicating capacity is still tighter than a year ago.

Dry vans remained the dominant equipment type on Loadlink at 54% of postings, followed by reefers at 23% and flatbeds at 18%. Reefer activity reached its highest share of the year as produce season ramped up.

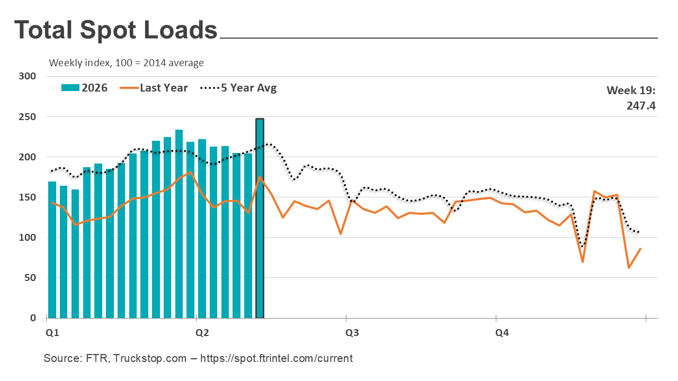

Market conditions tightened dramatically during the week ending May 15 as International Roadcheck inspections disrupted capacity across the spot market.

Truckstop.com reported total load activity jumped 21% week over week — the largest increase of the year — as many drivers avoided enforcement activity and more freight shifted into the spot market.

Spot market truck postings fell 8.5% during the same week, the largest weekly decline since January, while the market demand index — measuring the ratio of loads to trucks — climbed to its highest level in five years.

Reefer spot rates posted their largest week-over-week increase ever during Roadcheck week, according to truckstop.com, while dry van rates narrowly missed a record weekly gain. Flatbed spot rates rose for a 20th consecutive week to a record high.

Analysts continue to caution that broader uncertainty tied to tariffs, fuel prices and freight fundamentals could still limit a sustained market recovery.

DAT noted that spot-contract spreads have narrowed considerably since late 2025, not because of surging freight demand, but because available truck capacity continues shrinking faster than freight volumes.

Have your say

This is a moderated forum. Comments will no longer be published unless they are accompanied by a first and last name and a verifiable email address. (Today's Trucking will not publish or share the email address.) Profane language and content deemed to be libelous, racist, or threatening in nature will not be published under any circumstances.