ATA’s Costello says trucking’s ‘painfully slow’ recovery driven by shrinking capacity, not freight demand

Fleets attending the Truckload Carriers Association (TCA) annual convention in Orlando, Fla., last week were eager for Bob Costello’s economic outlook update for 2026, hoping to hear the long-anticipated news of broad freight market recovery and increased demand.

However, the American Trucking Associations (ATA)’s chief economist and senior vice president had a different message: not so fast. “Here comes the cold water…sort of,” he said less than a minute into his presentation.

While the industry is beginning to see signs of improvement after a prolonged freight downturn, Costello cautioned that optimism and the change fleets are feeling is because “we are absolutely moving in the right direction” when it comes to supply, not because of a surge in freight demand.

“The supply side is absolutely real, and that’s why you’re starting to feel better. It’s not coming from the demand side of freight. And I think you all have to remember that,” he said. “Because what does this industry almost always do when things start to get better? Start buying trucks. And what I’m here to tell you is, I don’t think there’s going to be a lot more freight out there to support it if everybody starts doing that.”

Tariffs, tariffs, tariffs

Costello said the broader U.S. economy remains stable, and he does not expect a recession, but the sectors that matter most for trucking are not showing strong momentum.

Economic growth continues to hover near its long-term trend of about 2%, but two-thirds of that GDP is coming from services.

“You’re not putting services in trailers. You’re putting goods in trailers. And we need to focus on that side of the economy,” Costello said, adding that in Q4 2025 goods consumption contributed very little to GDP growth.

“We’re not getting the swell of new demand coming up for freight,” Costello said. “This is really a supply-side story.”

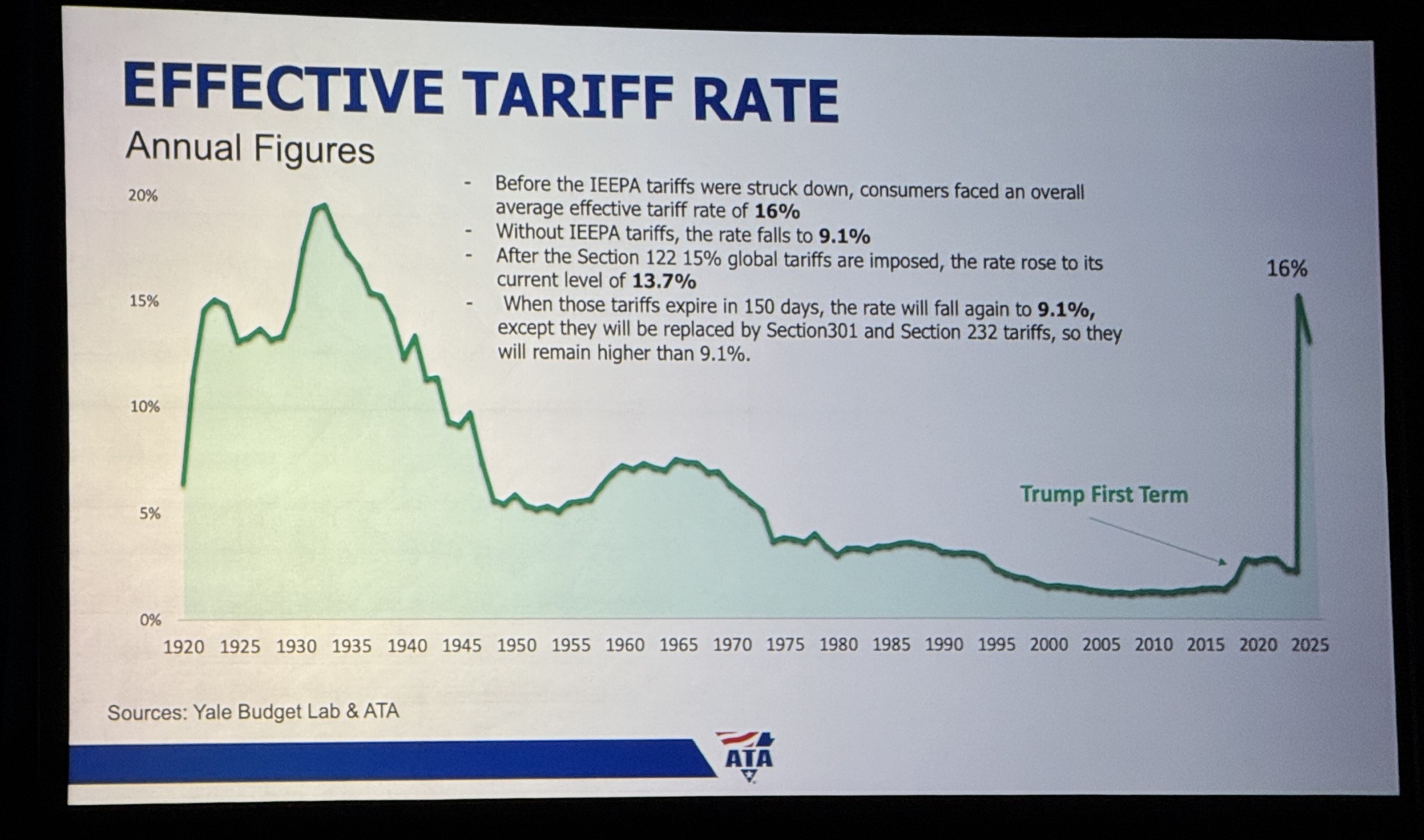

And tariffs are a part of why the demand for goods has been stalled, as U.S. tariff levels are now the highest they have been since the 1930s. And while the current administration is expected to lower some rates slightly — from roughly 16% to about 14% — Costello said most tariffs are likely to remain in place in some form.

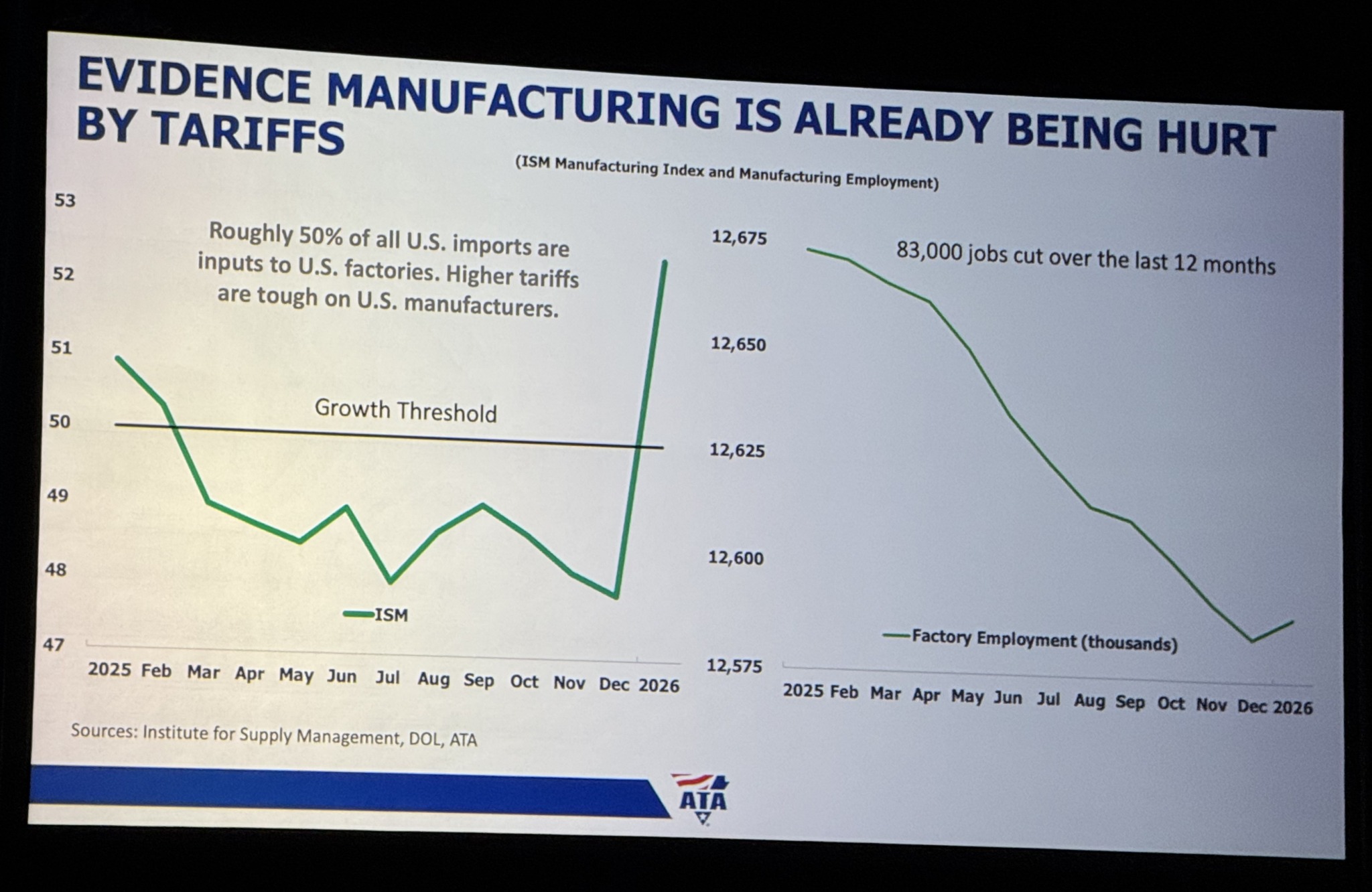

He explained that while tariffs are often associated with finished consumer goods, roughly half of all imports entering the U.S. are actually inputs used by domestic manufacturers to assemble finished goods. These headwinds have already led to a decline of about 83,000 manufacturing jobs over the past 12 months.

Overall factory output increased just 1.1% last year. “Not great, but certainly not terrible,” Costello said. But a closer look at the data shows that most of that growth was concentrated in just a few sectors.

Aerospace, which accounts for roughly 4% of total U.S. manufacturing production, posted strong gains. Computer and electronic equipment — representing about 4.5% of production — also saw significant growth. “Combined, aerospace and computer and electronic equipment are less than 10% of total production,” Costello said. “If you’re hauling for them, that’s fantastic.”

Chemicals, the second-largest manufacturing category after food and beverages, also increased production by about 3.3%. But outside those industries, manufacturing output was weaker.

“If you take those three areas out of total production, guess what? It was down. So you can certainly find some pockets of strength on the manufacturing side, but it is not across the board.”

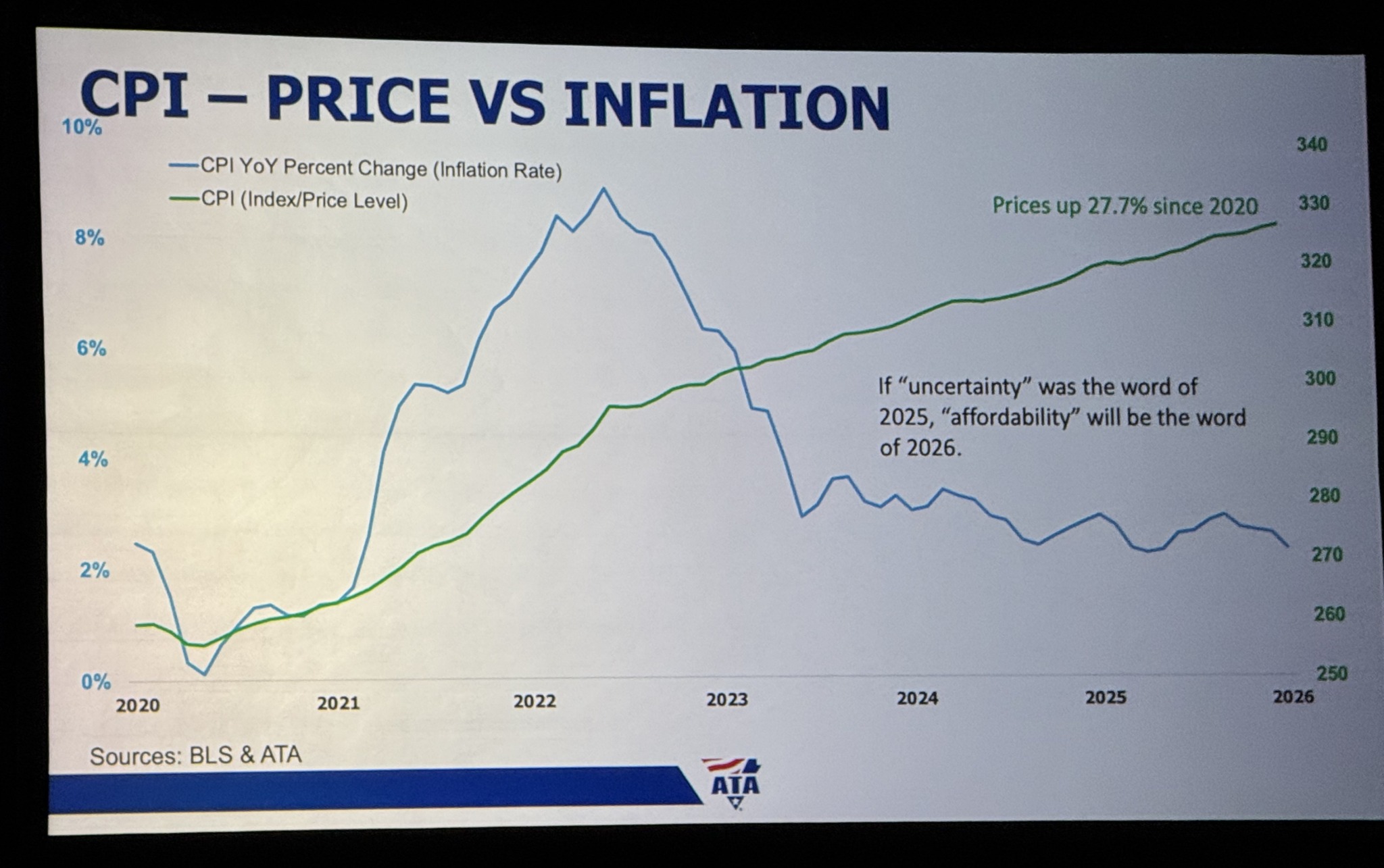

Affordability will be the word of 2026

If uncertainty was the word of 2025, affordability will be the word of 2026, Costello said, as consumers are also feeling the effects of tariffs and rising prices.

While the consumer price index (CPI) recently rose about 2.4% year over year, close to the Federal Reserve’s target, suggesting inflation is largely under control, overall price levels remain significantly higher than before the pandemic. Producer prices are also worth watching, Costello said. “The Producer Price Index (PPI) surged in January. That’s usually a precursor to consumer prices. Keep that in mind and remember that.”

Prices have increased by almost 28% since 2020. Such an increase in everyday goods limits discretionary spending, weighing on freight demand tied to retail.

Costello described the economy as “K-shaped,” with the top 20-25% of households continuing to spend as they did before, while the remaining majority feel far more constrained by rising prices. While some believe cutting interest rates would solve the issue, surveys still show customers are more concerned by prices than interest rates.

Slower job growth is also weighing on consumer spending. While the U.S. unemployment rate sits around 4.3%, Costello noted job creation has slowed a lot, averaging just about 15,000 new jobs per month in 2025 compared with roughly 183,000 before the pandemic. The second half of 2025 averaged at just more than 3,000.

Freight indicators show early signs of stabilization

The good news is that while truckload volumes remain below previous peaks, conditions have begun to improve slightly.

Contract truckload shipments increased 1.4% in January on a seasonally adjusted basis — the strongest monthly gain since October 2024. However, it was down 1.9% in 2025, with a 3.5% year-over-year decrease in Q4. January 2026 saw a 1.6% decline compared to a year ago.

However, volumes remain well below earlier highs. January contract loads were still about 9.2% below the 2022 peak.

Spot market activity has shown stronger momentum, with load postings rising 20.5% year over year in 2025 and accelerating toward the end of the year, rising 24.6% year over year in the fourth quarter and 29.2% in January.

Because the spot market typically reacts first when capacity tightens, improvements there could eventually feed into contract rates, Costello suggested.

Less-than-truckload (LTL) indicators tell a similar story of gradual stabilization. LTL shipment counts increased about 2.4% year over year in January, suggesting freight activity is beginning to pick up. However, tonnage remains down (-3.6% year over year in January), meaning the average weight per shipment is still falling.

Regional freight data also suggests the market is stabilizing unevenly across the country.

The Northeast — one of the regions hardest hit during the freight downturn — has begun to show improvement. The West Coast remains relatively stable, while the Southwest, which had been one of the strongest markets earlier in the cycle, is now beginning to slow.

Meanwhile, freight activity in the Midwest and Southeast remains down compared with previous highs but has improved compared with last year.

“In all cases, 2025 was better than 2024,” Costello said.

Cross-border freight flows softened, too. Truck traffic entering the United States from Canada declined about 5.1% last year, while inbound truck traffic from Mexico also declined, though by 0.4%. Although the drop from Mexico was small, it marked the first non-recession decline since 2003, suggesting that tariffs and shifting trade policies may be beginning to affect cross-border freight flows.

Capacity leaving the market

Costello said the trucking industry has experienced what amounts to a form of “mini-stagflation” over the past several years, with operating costs rising even as freight rates stagnated or declined. Citing data from the American Transportation Research Institute, he illustrated the imbalance. Taking 2019 as a baseline — when revenue per mile roughly matched cost per mile — operating costs excluding fuel have since risen about 26% more than revenue.

“That’s unsustainable,” Costello said, concluding that the imbalance has forced capacity out of the market.

One of the clearest indicators is the declining number of carriers. In December last year, there were more than 42,000 carriers (11.6%) fewer carriers compared to December 2022.

Driver employment has also fallen. In general freight, local operations saw employment of company drivers fall 1.7% in 2024 and decline another 1.8% in 2025. The drop was even steeper in long-distance trucking, where employment declined 3.4% in 2024 and fell an additional 2.1% the following year. Specialized freight operations also experienced significant reductions two years ago, with employment falling 3% before a slight 0.7% increase in 2025.

As they are, these numbers could still be underestimating the number of drivers leaving the industry, as Costello said that the Department of Labor recently revised its driver employment estimates downward by roughly 15,000 drivers after finding out that earlier counts were overstated.

Costello added that capacity reduction is not coming only from fleets and drivers exiting the market. Some of it may also come from the government enforcement efforts targeting cabotage, a misuse of B1 work visas. That visa allows international drivers to bring loads into and out of the United States, but it does not allow them to run regular domestic freight within the country. Yet some fleets – especially on the southern border — use B1 drivers for those internal moves, creating illegal ‘shadow’ capacity, Costello explained.

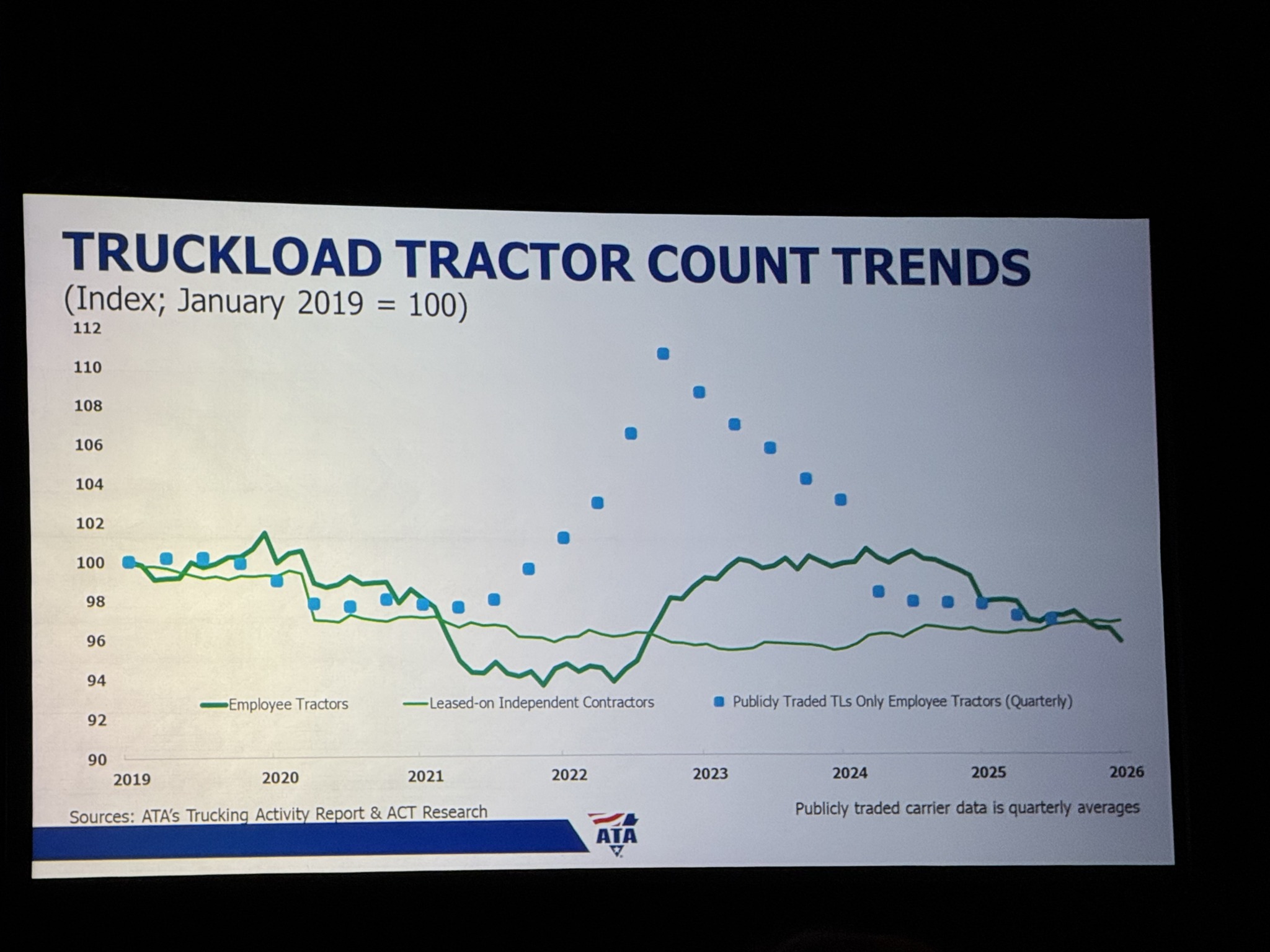

Truck and trailer trends

ATA data tracking truckload tractor counts show fleet sizes gradually shrinking from the highs reached during the pandemic freight boom. Both employee-operated tractors and leased tractors operated by independent contractors have trended downward since 2023, according to ATA’s Trucking Activity Report and ACT Research.

Publicly traded truckload carriers — which expanded during the pandemic surge in freight demand — have also been steadily reducing their tractor counts in recent quarters.

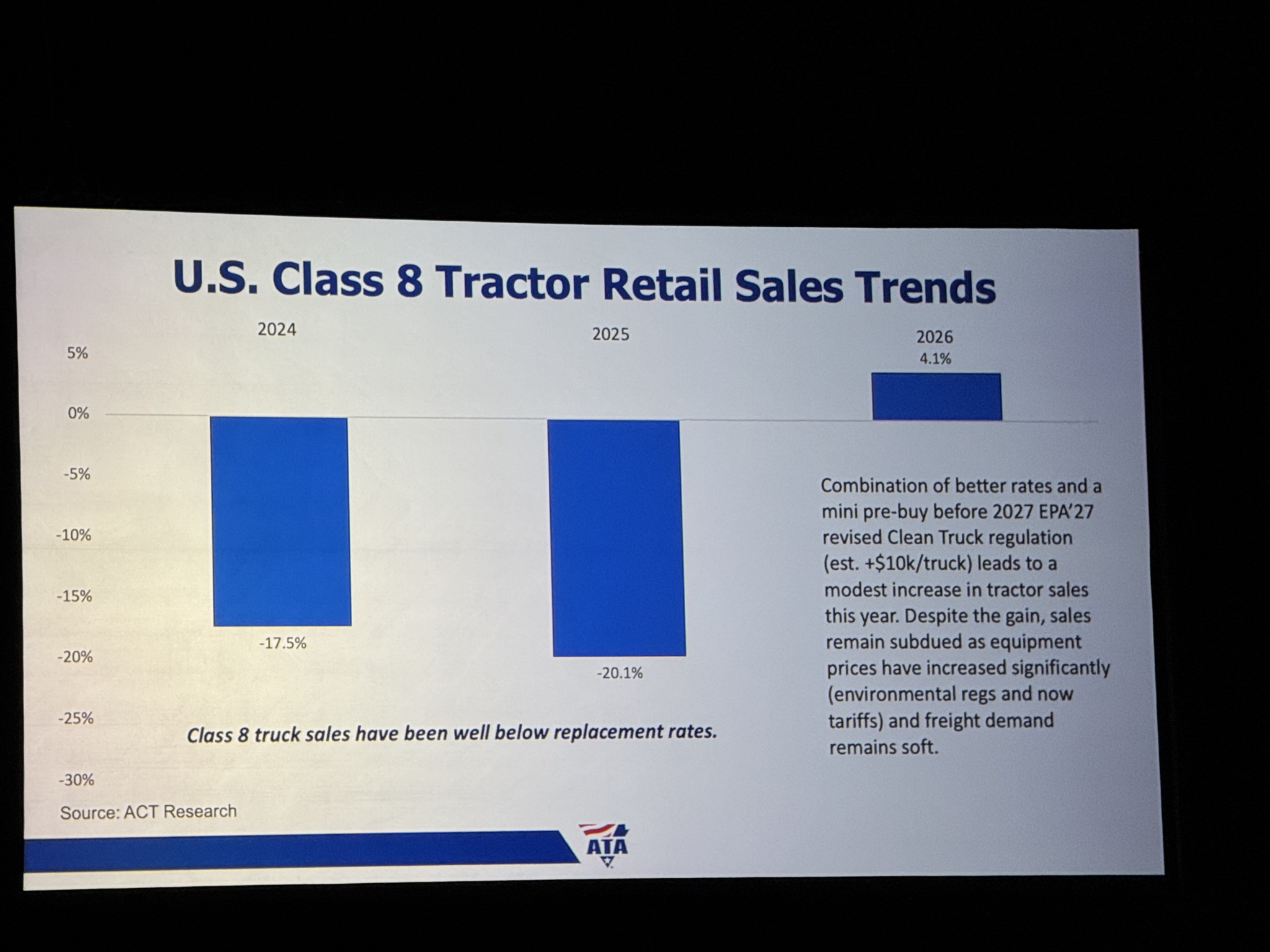

New truck purchases show the same pattern.

U.S. Class 8 tractor retail sales fell sharply during the downturn, declining about 17.5% in 2024 and another 20.1% in 2025. The drop has pushed equipment purchases well below normal replacement levels, meaning fleets have been shrinking or aging their equipment rather than expanding capacity.

Costello expects a modest rebound this year, with sales projected to rise about 4.1%. The increase will likely be driven by a combination of slightly improving freight conditions, routine fleet replacement, and a small pre-buy ahead of EPA’s 2027 emissions regulations. But after two consecutive years of steep declines, even a small increase in orders is unlikely to significantly expand capacity.

In his final message to attendees, Costello said that fleets have the right to be cautiously optimistic.

“Demand-based recoveries are easy, right? All of a sudden, you just get a bunch of new freight. That’s probably not what we’re going through,” he said. “Supply-based recoveries are more difficult, but it is happening. It’s slower. It’s painfully slow. It takes a while, but it is happening…We are in a recovery… I’m already sensing you’re feeling better, and I think that will continue through much of this year as a result.”

Have your say

This is a moderated forum. Comments will no longer be published unless they are accompanied by a first and last name and a verifiable email address. (Today's Trucking will not publish or share the email address.) Profane language and content deemed to be libelous, racist, or threatening in nature will not be published under any circumstances.

-

That was ATA more than TCA. Especially the driver shortage narrative and their push for self certification of CDL schools.

This group caused the surplus of trucks and truck drivers and screamed a truck driver shortage.