ECONOMIC TRUCKING TRENDS: Class 8 orders drop as spot market rates reach record highs

Class 8 orders fell sharply in April, but analysts say a drop was expected due to seasonal norms.

Spot market rates remain a bright spot for truckers, outpacing increases to diesel prices and establishing new record highs.

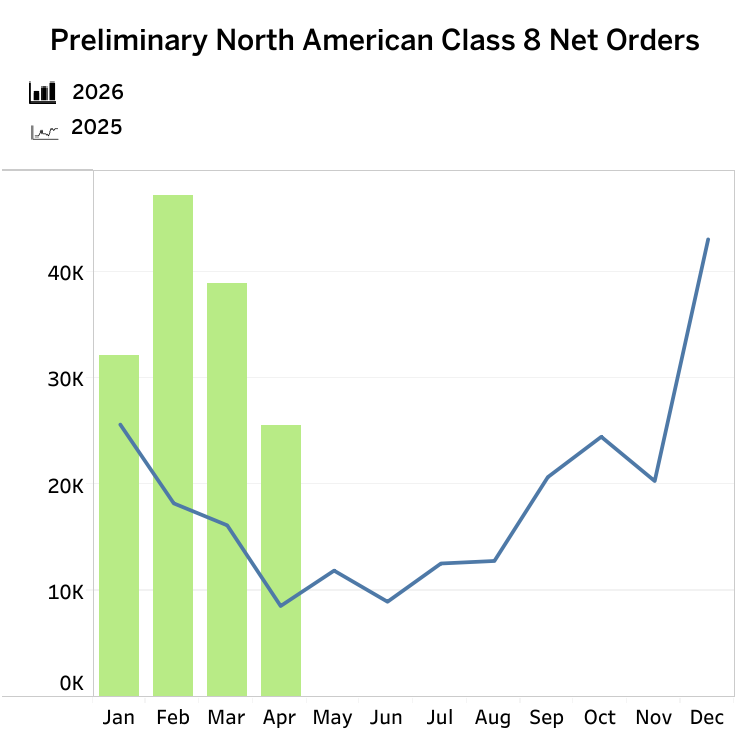

Class 8 orders drop sharply

Class 8 orders plunged 34% in April to 25,500 units, according to preliminary data from FTR, but were up 199% year over year against a weak April 2025.

Orders have now totaled 298,105 units over the past 12 months, FTR reported. It chalked up the drop-off to seasonal trends.

Orders for 2026 are now up 110% year over year, thanks to firmer freight rates, tightening capacity, higher fleet utilization and growing replacement needs.

FTR is now calling for a moderate pre-buy as EPA27 cost increases approach.

“The abrupt shift in demand in recent months has brought some risks as we have noted previously. One risk is that fleets will act out of ‘fear of missing out,’ or FOMO, to order earlier or in larger quantities than needed to avoid being shut out of 2026 production, thus raising cancellation risks. We still believe that risk is limited unless freight recovery stalls,” said Dan Moyer, FTR’s senior analyst, commercial vehicles.

“The more notable risk from elevated orders is build execution. Demand is very strong, but OEMs and suppliers must now ramp production from a low Q1 base without creating labor, supply chain, quality, or inventory issues.

“Other risks remain, including uncertainties over regulatory policy and the durability of the freight recovery, elevated financing costs, and geopolitical developments that could keep fuel prices elevated. Overall, April orders reinforce the main message: Class 8 demand remains strong, but the focus is shifting from demand recovery to backlog quality and production execution.”

ACT Research reported 24,800 orders, a 201% year over year increase.

“With April signifying the beginning of weak order seasonality until 2027 order boards open in September, it’s little surprise that preliminary April Class 8 order activity fell from March levels,” said Carter Vieth, research analyst at ACT Research. “Seasonally adjusted, Class 8 orders declined 24% month over month.”

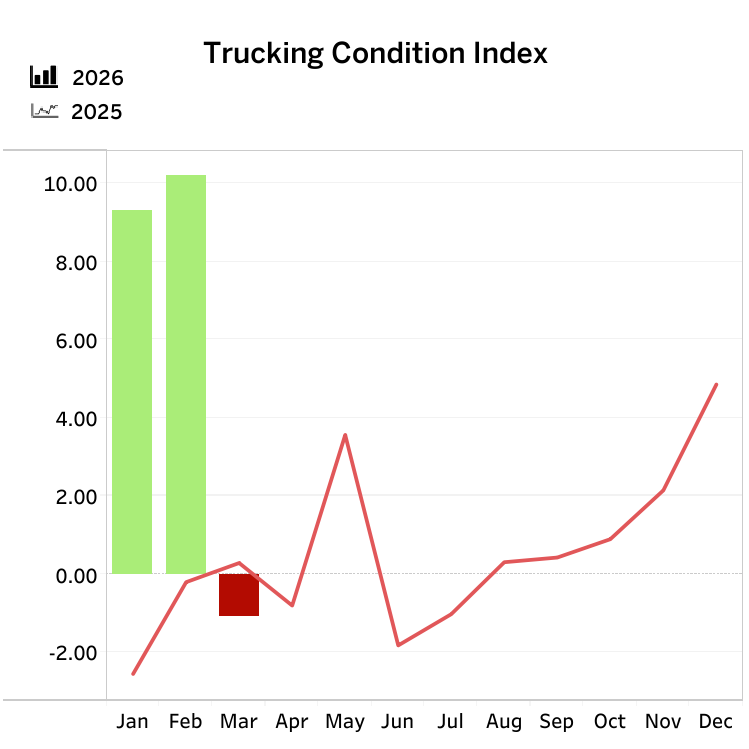

Trucking conditions worsen…but likely briefly

Surging diesel prices worsened trucking conditions, according to the FTR Trucking Conditions Index, which dropped from a four-year high reading of 10.2 in February back to negative territory at -1.11 in March.

However, Avery Vise, FTR’s vice president of trucking, said rising rates are offsetting higher fuel costs, so the outlook remains “solidly favorable” for carriers.

“Carriers of all stripes are in store for a strong year from a rates perspective, but for much of the market, the recovery remains driven by the combination of very tight capacity and disruption,” said Vise.

“We are still skeptical that van freight will benefit much from volume growth, but the open deck sector is benefiting not only from very tight capacity but also from an ongoing surge in data center construction and a modest improvement in manufacturing output.”

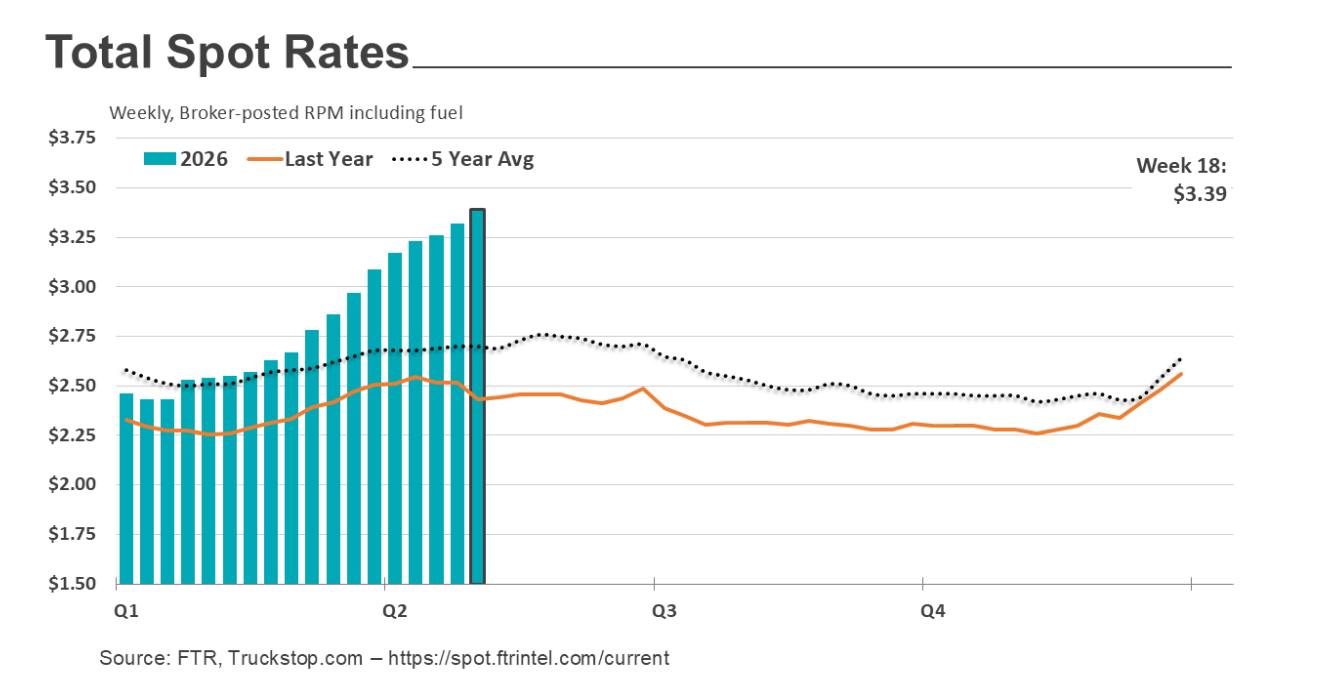

Spot market rates continue to rise

Truckstop.com and FTR reported spot market rates were up across all equipment types for the week ended May 8, with total market rates setting a new record.

Flatbed rates climbed for the 19th straight week, just a tenth of a cent per mile below their record high.

Dry van rates hit their highest mark since April 2022, while reefer rates were softer and haven’t yet matched levels seen at the end of 2025.

Have your say

This is a moderated forum. Comments will no longer be published unless they are accompanied by a first and last name and a verifiable email address. (Today's Trucking will not publish or share the email address.) Profane language and content deemed to be libelous, racist, or threatening in nature will not be published under any circumstances.