Economic Trucking Trends: More ‘rough sledding’ ahead, trailer orders plunge

It looks like the trucking industry will end 2023 on a soft note, according to the latest data we’ve come across. U.S. for-hire truck tonnage slipped in November, trailer orders plunged, but falling diesel prices offered truckers some mild relief.

ACT Research advises to buckle in for more “rough sledding” as the industry continues to add equipment (thank private fleets for that). Turning to the spot market, van rates were weak, but flatbed and specialized segments showed some strength in the most recent week.

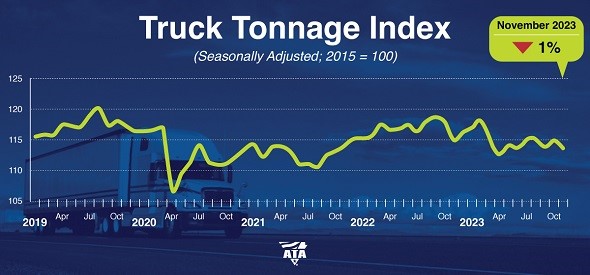

Truck tonnage slipped in November

U.S. for-hire truck tonnage dipped 1% in November, giving up the revised 0.8% increase it saw in October, according to the latest data from the American Trucking Associations (ATA).

“We continued to see a choppy 2023 for truck tonnage into November,” said ATA chief economist Bob Costello. “It seems like every time freight improves, it takes a step back the following month. While year-over-year comparisons are improving, unfortunately, the freight market remains in a recession. Looking ahead, with retail inventories falling, we should see less of a headwind for retail freight, but I’m also not expecting a surge in freight levels in the coming months.”

The seasonally adjusted index was down 1.2% compared to last November. If you’re keeping score at home, that’s nine straight month of YoY decreases.

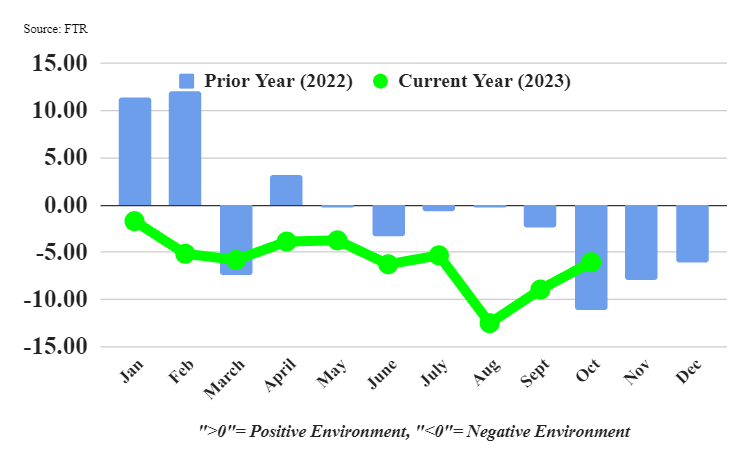

Trucking conditions improve, remain difficult

Industry forecaster FTR’s Trucking Conditions Index climbed to -6.07 in October, reflecting improvement from its -8.97 reading in September. Improvements came mostly in the form of falling diesel prices, but conditions remain difficult for carriers, FTR reported.

“The decline in diesel prices represented the only positive contribution to October’s TCI, although rates and cost of capital were less-negative factors than they had been in September,” said FTR’s vice-president of trucking, Avery Vise.

“As we have discussed frequently, the combination of stagnant freight volume and surprisingly resilient capacity is thwarting a near-term turnaround for the truckload sector. Our analysis suggests that market conditions for carriers will not start to recover until the second half of 2024 absent an acceleration in the current rate of capacity loss.”

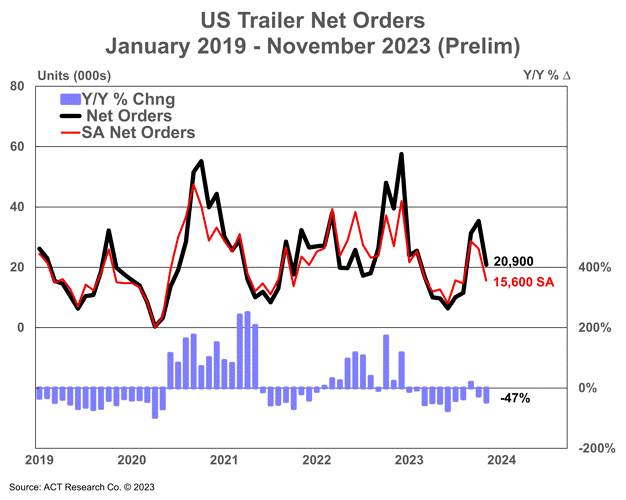

Trailer orders plunged in November

November net trailer orders plunged by more than 13,000 units in November, to 21,362 units, according to data from FTR. Orders were off 38% from October and 45% year over year.

“With orders coming in under production levels, backlogs in November fell slightly, shedding almost 2,500 units to end at just over 140,000 units,” said Eric Starks, chairman of FTR. “The more pronounced fall in production resulted in an increase for the backlog-to-build ratio to 5.9 months. This ratio is in line with the historical average prior to 2020 and suggests the industry is moving towards a pre-pandemic level of stability.”

“Not only were orders down materially from year-ago levels, but preliminary net orders, at 15,600 seasonally adjusted, were about 41% lower sequentially,” added Jennifer McNealy, director of commercial vehicle market research and publications at ACT Research. “After two months with orders above 30,000 units, it’s certainly disappointing, although not unexpected, to see orders drop, particularly amid a backdrop of weak profitability for truckers and anecdotal commentary from trailer manufacturers who have shared that orders are coming but at a slower pace than they have the last few years.”

McNealy cautioned that one month of lower orders “doesn’t indicate a catastrophic year in the offing.”

“Other indicators being watched closely include cancellations, which have returned to acceptable levels for most segments of the industry, and the backlog-to-build ratio, which in aggregate remains healthy at nearly six months,” she concluded. “Some specialty segments have no available build slots until late in 2024 at the earliest.”

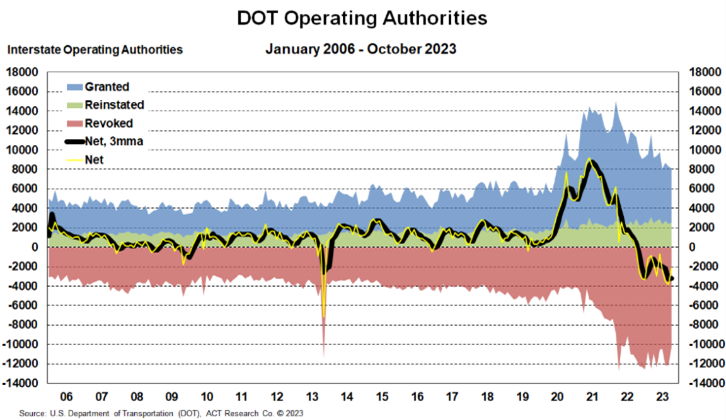

Trucking capacity remains excessive

ACT Research, in its latest Freight Forecast, U.S. Rate and Volume Outlook report, warned that capacity expansion is threatening to keep conditions difficult for carriers.

“Capacity expansion continues to pressure the for-hire market, as the industry still collectively ignores the first rule of getting out of a hole: to stop digging,” said Tim Denoyer, ACT Research’s vice-president and senior analyst. “In addition to falling pent-up capital spending, low freight rates are driving net revocations of operating authorities to a record pace, so we expect this to shift next year.”

ACT reported the spot market continues to have too much capacity, and private fleets continue to add equipment. As a result, expect “at least a few more months of rough sledding,” ACT warned.

“Consumer purchasing power is improving with significant disinflation and solid wage growth driving improving retail sales trends, which will push the inventory cycle forward. And as the industry right-sizes, tighter capacity should eventually start to push truckload spot rates higher,” Denoyer said. “In an early sign of better cyclical demand in 2024, container imports and intermodal volumes have returned to growth, with global ocean constraints at both the Panama Canal and the Suez Canal pushing freight to west coast ports.”

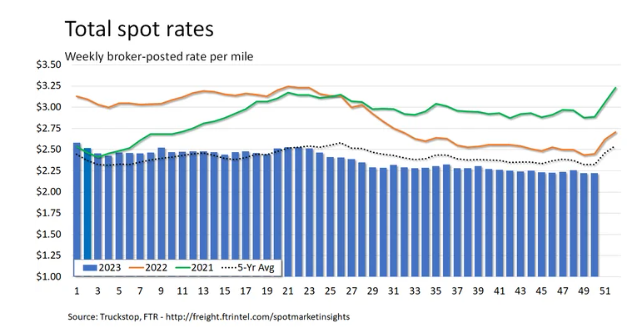

Van spot rates slide further

The week ended Dec. 15 showed lower-than-average rates and volumes, according to Truckstop and FTR Transportation Intelligence.

The outlier was the flatbed segment, where rates came in higher than the refrigerated and van segments. Rates for specialized equipment saw their strongest increase since August. Generally, van rates spike for the final two weeks of the year, but no such luck this year, Truckstop reported.

“The fact that the current week ends a couple of days before Christmas Eve could moderate the usual dynamic this week,” it said. “However, if that occurs, the first week of 2024 could see rate increases instead of decreases, which are more common.”

The Market Demand Index fell slightly to 49, as the addition of truck postings surpassed load postings.

Have your say

This is a moderated forum. Comments will no longer be published unless they are accompanied by a first and last name and a verifiable email address. (Today's Trucking will not publish or share the email address.) Profane language and content deemed to be libelous, racist, or threatening in nature will not be published under any circumstances.

In March of 2021 and again in March of 2022 we said we should limit foreign drivers from lower wage countries to 1 month permit to bring their license upto standards and a 8 month work permit from April to December 15 of 2021 and again of 2022

We said we did not have enough housing for these truck drivers to bring their family in

We need a plan like the U K and Holland are doing that imported workers or foreign students that switch to truck drivers must make at least $25 hr plus medical coverage after they have been driving in Canada 8 months

We also need a plan that all the foreign workers families have housing if employers want to sponsor or keep those workers in Canada. This was predicted that a surplus of trucks and drivers would cause many more people to become homeless who worked in transportation or their children. I volunteer at a homeless tent encampment

Our big help comes froma membership based co when red stripes on the warehouse