Economic Trucking Trends: Slowing Class 8 sales could cause OEs to curtail production

The first half of January 2024 is nearly in the books, and with it comes news that shippers are loving life thanks to lower fuel costs and other improving metrics that have pushed the FTR Shipper Conditions Index further into positive territory.

Truckers on the spot market saw volumes surge in the first week of the year, but rates declined as is normal for the week. Those rate declines, however, were more subtle than usual.

And truck OEMs may put the brakes on production as weakening demand and still robust build rates threaten to create an inventory glut they’ll be motivated to prevent.

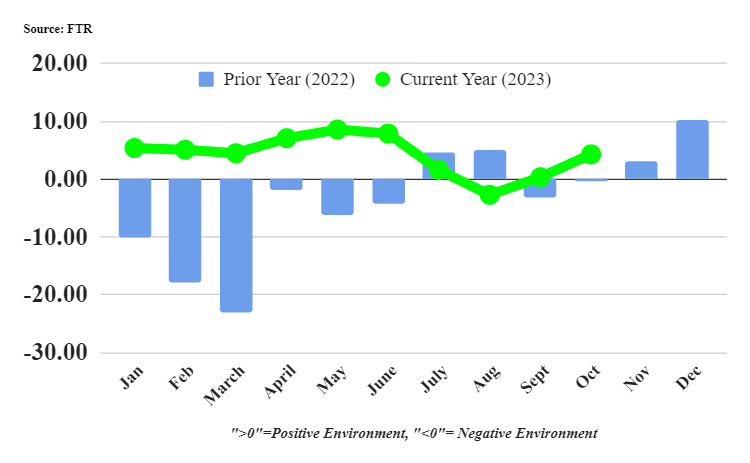

Shipper conditions improve sharply

Shippers saw conditions improve in October from a barely positive reading of 0.35 in September, to 4.3. This, according to the Shippers Conditions Index compiled by industry forecaster FTR.

Thank lower diesel prices for the improved conditions, FTR reported, though all other major factors were also at least marginally more favorable in October than in the previous month.

“Overall market conditions for shippers in October as measured by the SCI were the most favorable since June, but swings in fuel costs largely have been the variable month to month,” said FTR vice-president of trucking, Avery Vise.

“Key freight dynamics – rates, utilization, and volume – have been mostly stable over the past several months and look to be so for at least a few months of 2024. After the boosts from falling diesel prices in November and December 2023, we expect market conditions for shippers to soften gradually, but we do not foresee significantly negative conditions during the forecast horizon.”

Could truck makers pump the brakes on production?

ACT Research reports conditions are aligning for truck manufacturers to create a Class 8 inventory surge, which may cause them to curtail production. Continued strong build rates combined with fading U.S. tractor demand, and seasonal risks combine to create this potential scenario.

Class 8 inventory accumulated in October and November by 4,300 units, ACT reports, which is more than the 3,300 units accrued across the previous 12 months.

“Something we marveled at, as late as this September, was the close correlation between build and sales that had kept Class 8 inventory levels, both nominal and relative, near perfectly positioned very late into the cycle,” said Kenny Vieth, ACT’s president and senior analyst. “Increasingly, with inventories already rising and the sales calendar becoming unfriendly in early 2024, the data suggest this cycle will not provide an it’s different this time outcome, with more inventory accrued in the last two months than the preceding 12 months.

“The Class 8 forecast has anticipated a production slowdown beginning in Q1. As any significant inventory stockpiling won’t occur until January and February, we are probably early in our call for build rate cuts sooner. The U.S. Class 8 tractor sales rate has been trending lower since Q2 2023, and even in good markets, January and February are far and away the worst months of the year for retail sales.”

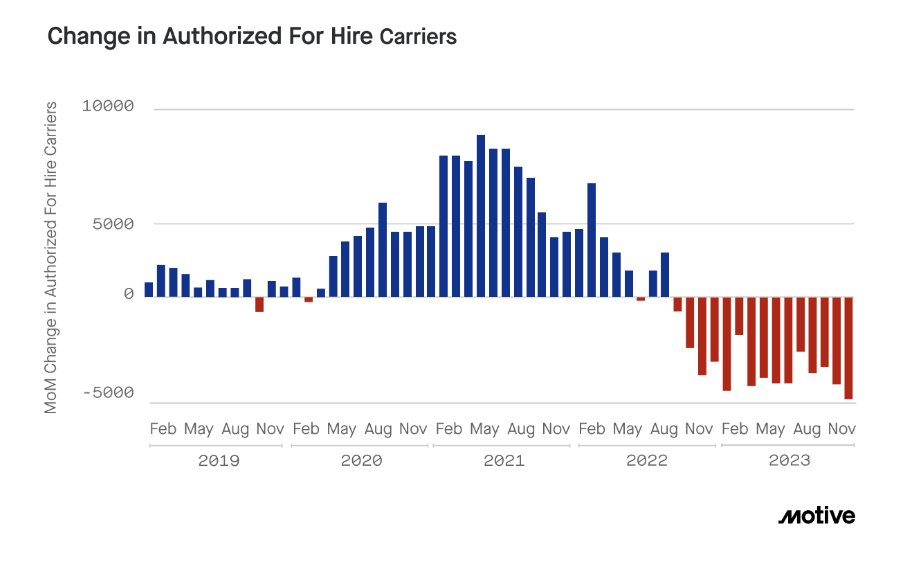

Capacity cull continues in December

In its latest monthly economic report for December, Motive reported the highest levels of carrier exits and lowest number of new carrier registrations for the year coming in the final month. This even though its Big Box Retail Index (measuring the number of truck trips to major retail DCs) peaked in December and fuel prices continued to decrease.

“Motive predicts that this contraction of the freight market will continue in early 2024, but retail trends and economic factors indicate we may see less volatility in the second half,” Motive reported.

Taking a deeper look, there were 4,860 carrier exits in December, a 52% increase in closures compared to the average seen through 2023. It was also the fourth consecutive month of slowing carrier registrations, which were down in December by 4%, or down 42% compared to December 2021 when freight demand was still strong.

“After three years of impacts from the pandemic and major external forces disrupting the freight market, 2024 may be the first time carriers will get a sense of what the new normal will look like,” Motive reported.

“Retailers are restocking inventories again, potential interest rate cuts could mean better access to capital, and consumer demand could be less volatile if inflation keeps cooling. While we will likely continue to see overall contraction of the freight market, we expect that 2024 will be less volatile, creating more predictability in freight and inventory planning.”

Spot volumes surge to start 2024, but rates soften

There was a surge of spot market load availability in the first week of 2024. Truckstop reported load postings were up 51.7% for the week ended Jan. 5 (compared to a holiday-shortened prior week), while truck postings rose just 7%, pushing the Market Demand Index up 21 points to 71.3.

But rates fell 3.1%, down 10.8% year over year. Broker-posted rates in the Truckstop system always fall during the first week of the year, Truckstop noted, but this year’s decrease was the smallest for the week since 2018.

Total load volumes were down about 28% year over year, and 37% off the five-year average. Total rates slid about 7.4 cents a mile after rising 10 cents the previous week, and were nearly 11% below the same week in 2023.

Have your say

This is a moderated forum. Comments will no longer be published unless they are accompanied by a first and last name and a verifiable email address. (Today's Trucking will not publish or share the email address.) Profane language and content deemed to be libelous, racist, or threatening in nature will not be published under any circumstances.