Carriers cut insurance coverage as premiums soar, ATRI report reveals

Carriers have been decreasing insurance coverage levels, raising deductibles and self-insurance retention levels, and decreasing investments in other cost centers, a new report revealed.

The American Transportation Research Institute (ATRI) Thursday released a report analyzing trucking industry impacts from the rising costs of insurance.

ATRI found that despite increased liability exposure, out-of-pocket incident costs and carrier crash involvement remained stable or decreased among a majority of respondents.

The analysis utilized detailed financial and insurance data from dozens of motor carriers and commercial insurers. The report assesses immediate and longer-term impacts that rising insurance costs have on carrier financial conditions, safety technology investments and crash outcomes as well as strategies used by carriers to manage escalating insurance costs.

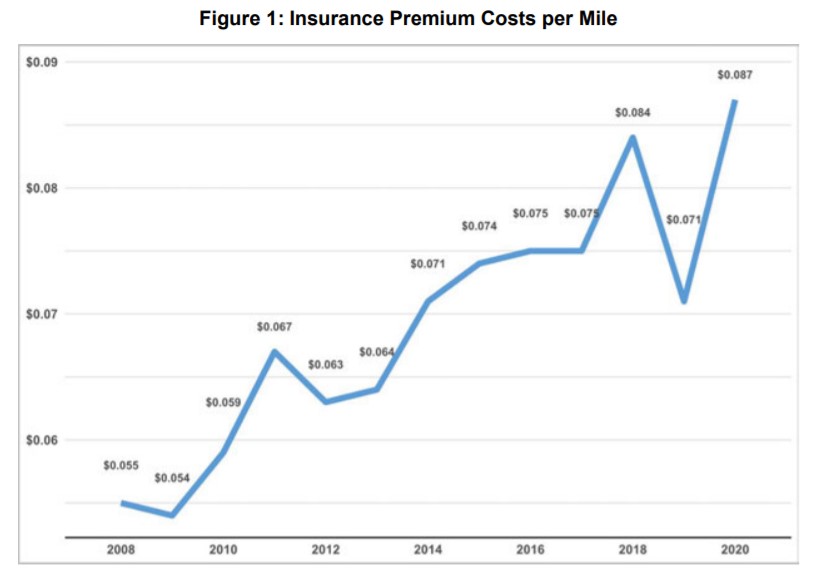

Despite reductions in insurance coverage, rising deductibles and improved safety, almost all motor carriers experienced substantial increases in insurance costs from 2018 to 2020.

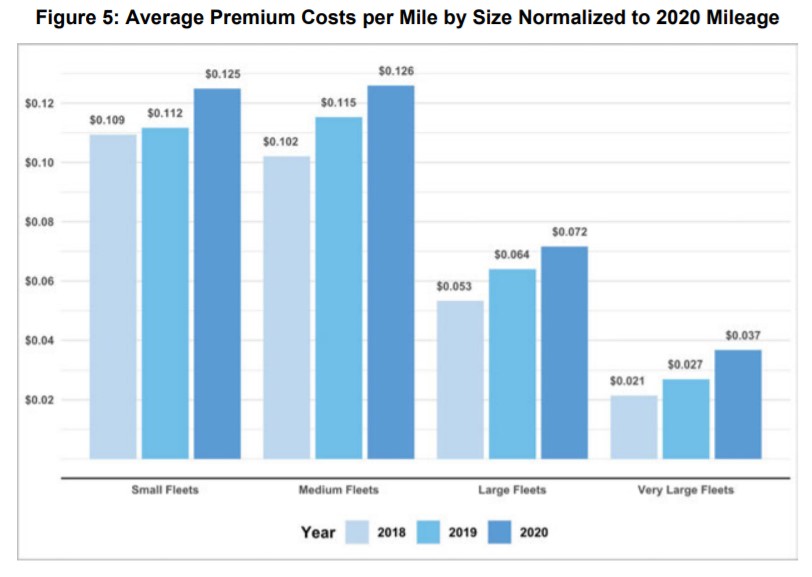

Premiums increased across all fleet sizes and sectors, with small fleets paying more than three times as much as very large fleets on a per-mile basis.

ATRI’s report on The Impact of Small Verdicts and Settlements in the Trucking Industry found that this category of litigation resulted in an average payment of between $406,386 and $449,792.6. Factors related to the litigation process – rather than crashes themselves – have a statistically significant impact on payment amounts.

Cases in highly litigious states such as California, Michigan, New Jersey, and North Carolina, for example, “had average litigation payments over 50% larger than the national average.”

Reductions in the coverage limits offered by insurers also force carriers to seek other sources of coverage or to operate with greater exposure to nuclear verdicts.

Motor carriers have responded with a variety of strategies for restructuring insurance policies, improving safety and redistributing operational costs.

Insurance costs are not the only costs on the rise, however. The new technologies that help make trucks safer, the bonuses or higher wages that promote safe driver practices, and the administrative initiatives to develop more comprehensive safety training and legal protocols have all led to higher marginal costs.

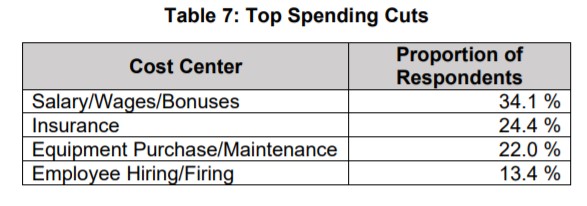

One-third of respondents reported cutting wages or bonuses due to rising insurance costs, and 22% cut investments in equipment and technology – potentially creating future safety and driver shortage concerns.

However, in the short-term, crash data confirms that carriers that raised deductibles or reduced insurance coverage were generally incentivized to reduce crashes in the subsequent year.

Road-facing cameras have become a strategic tool for insurers, carriers and drivers as they provide irrefutable safety documentation, thus lowering claims and defense costs. Camera evidence allows insurers to immediately determine the empirical facts of an incident to determine the most efficacious response to legal action, whether settling or challenging in court, and to minimize costly back-and-forth engagements.

“ATRI’s study corroborates the Triple-I’s research on rising insurance costs and social inflation – that increased litigation and other factors dramatically raise insurers’ claim payouts,” said Dale Porfilio, chief insurance officer of the Insurance Information Institute.

“External factors that go well beyond carrier safety force commercial trucking insurance costs to increase, which then requires carriers to redesign their business strategies. The higher premiums ultimately tend to be passed along to consumers in the form of higher prices for goods and services.”

Have your say

This is a moderated forum. Comments will no longer be published unless they are accompanied by a first and last name and a verifiable email address. (Today's Trucking will not publish or share the email address.) Profane language and content deemed to be libelous, racist, or threatening in nature will not be published under any circumstances.

I think 2 cents / L of the carbon tax should be put into a insurance fund in each province to run a non profit insurance for buses wheelchair van and transport insurance for companies of under 100 units or run as a non-profit organization including intercity buses and transit. Also used for more parking with electric plugs when cost effective. High insurance costs are pushing out many small taxi, bus , and delivery companies in Ontario. It also means that farmers and part time truckers can not afford to operate older equipment for the peak season. Many of the people protesting I met at queens Park have been former owners ops or smaller trucking companies that can no longer afford insurance in Ontario.