ECONOMIC TRUCKING TRENDS: Trailer orders drop sharply, spot market reflects rising diesel costs

Trailer orders disappointed in February, dropping sharply from December-January totals and reflecting ongoing concerns about the freight market.

And while spot market rates continue to improve, they’re growing more slowly than diesel prices are rising, meaning more capacity could head to the exits if fuel prices remain elevated.

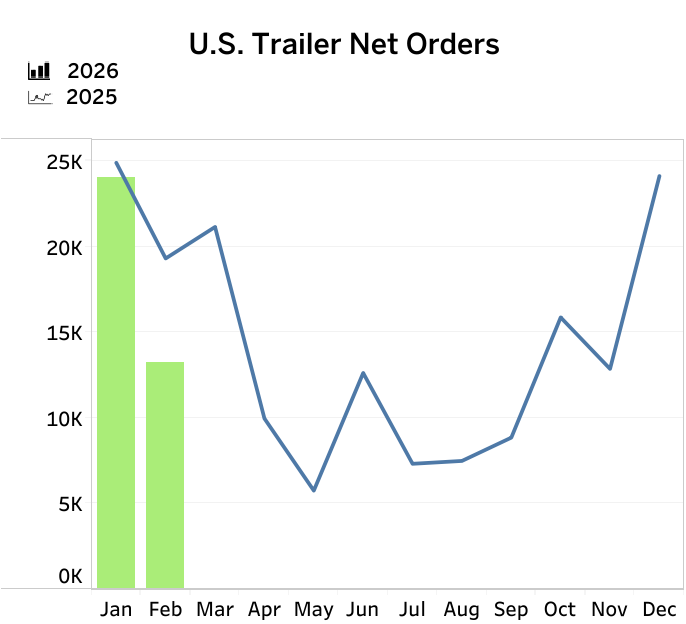

February order numbers throw cold water on trailer market

Consecutive months of strengthening trailer orders exceeding 24,000 units gave way to sharply lower orders in February totaling just 13,505 units, down 45% from the prior month.

They were also down 31% year over year, according to preliminary data from FTR, and were well off the 10-year February average of 25,172 trailers. That means the 2026 trailer order season (September 2025 to February 2026) is 19% softer than a year ago.

Demand remains at replacement level, FTR reports, while factors such as high steel and aluminum costs, ongoing tariff uncertainty, high financing costs and limited capital all weigh on the market.

“The U.S. trailer market remains under pressure from elevated input costs and ongoing trade uncertainty,” explained Dan Moyer, FTR’s senior analyst, commercial vehicles.

“Section 232 tariffs on steel, aluminum, and derivative products remain in place. Despite the U.S. Supreme Court’s February ruling striking down the administration’s country-specific tariffs that relied on emergency powers, replacement tariffs of 10% under other authority took their place. Trade pressures are also intensifying in the van segment due to an ongoing antidumping and countervailing duty investigation.”

ACT Research reported a 43% decline to 12,300 units.

“Sequentially, a drop in net orders was expected, as the industry transitions from the strongest to the weakest order months of the annual cycle,” said Jennifer McNealy, director commercial vehicle market research and publications at ACT. “Trailer makers now will begin to take fewer orders and start to work down the backlog that grew during the peak of order season at the end of the previous year, which in this year’s cycle started and ended later than usual, as fleet decision-making hesitance into late 2025 delayed the cycle a bit and caused a high-side surprise in January.”

She warned it may be a while before orders climb back above 20,000 units in a month, “particularly given concerns about the level of activity in the key freight-generating economic sectors that drive transportation demand.”

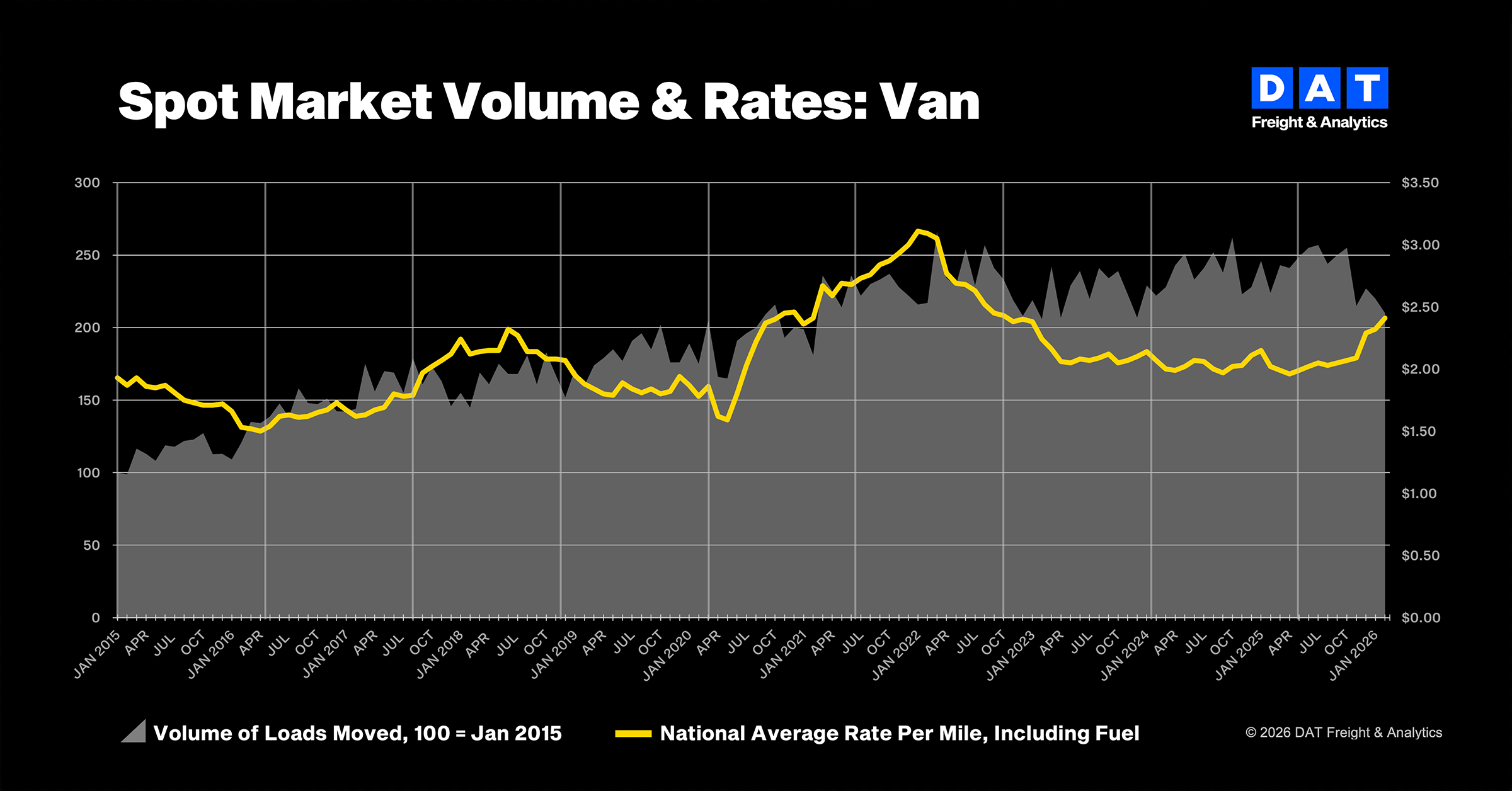

Truckload spot market rates post seventh consecutive monthly gain

Truckload volumes on the spot market softened slightly in February, according to DAT Freight & Analytics, but van and reefer rates posted their seventh straight month of gains.

Volumes declined by about 6% year over year in February.

However, van rates were up 9 cents/mile from January to $2.41, reefer rates climbed 7 cents/mile to $2.88 and flatbed rates spiked 14 cents to $2.72/mile.

Contract rates are also seeing some improvement, up 4 cents/mile, 8 cents/mile, and 12 cents/mile for van, reefer and flatdeck, respectively.

However, DAT says rising fuel prices tell part of the story, with the national average price for on-highway diesel rising to $3.71/gallon in February, up about 6% from January. Spot market prices generally do not include fuel surcharges and are likely to rise as the conflict in the Middle East puts further pressure on fuel prices.

“Without fuel hedging, contract pricing, or surcharges, carriers will need to negotiate higher spot rates now to compensate for higher pump prices,” said Ken Adamo, DAT chief of analytics. “Otherwise, more carrier exits are likely — which, paradoxically, could accelerate the supply-side market recovery.”

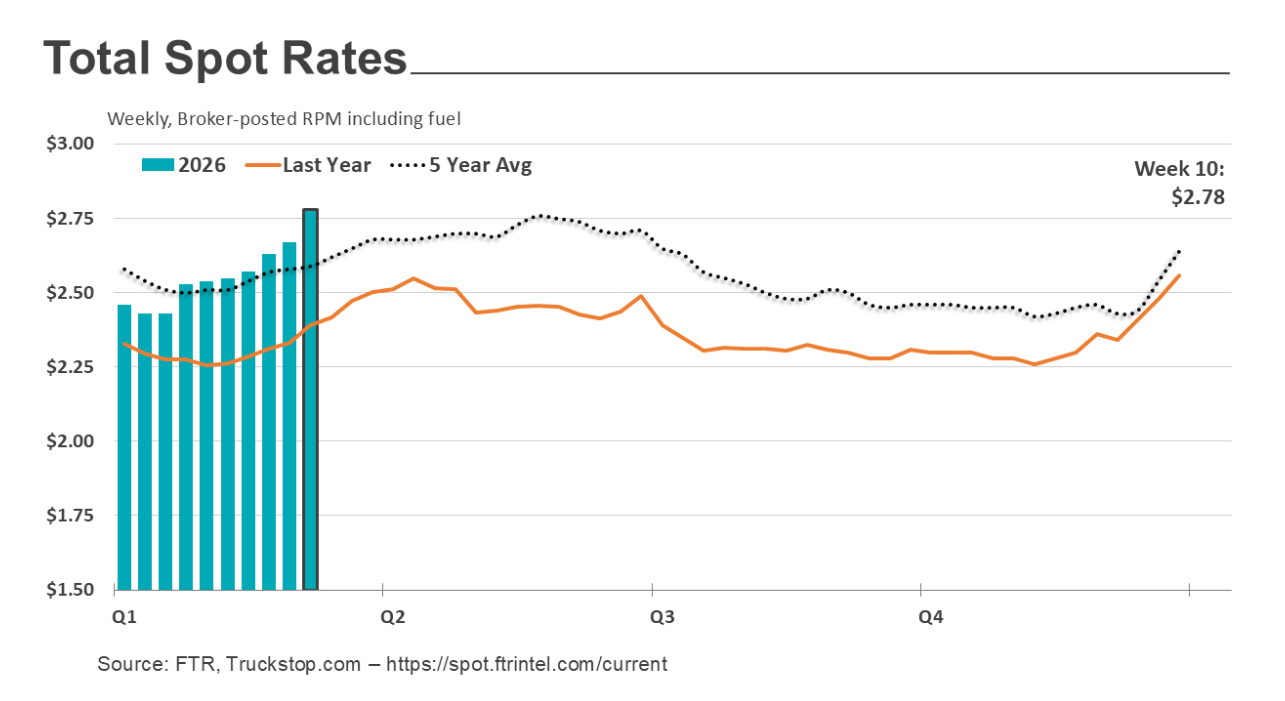

March rates reflecting those higher pump prices

For the week ended March 13, Truckstop.com and FTR reported that spot market prices are reflecting a 96.2 cent/gallon increase in diesel prices. FTR figures that has driven up carrier costs by about 16 cents/mile in just one week, pushing spot rates up about 10 cents/mile.

So, while spot market rates were up in the most recent week, carriers are worse off when considering the sharp spike in fuel costs.

“Total load postings rose to their highest level since June 2022. The increase in truck postings lagged the volume increase, and the Market Demand Index rose to 168.8 – the highest level in exactly four years,” Truckstop.com reported.

Have your say

This is a moderated forum. Comments will no longer be published unless they are accompanied by a first and last name and a verifiable email address. (Today's Trucking will not publish or share the email address.) Profane language and content deemed to be libelous, racist, or threatening in nature will not be published under any circumstances.