Uncertain but not anxious

Trying to figure out just how healthy the trucking industry is purely by juggling statistical data is an almost impossible trick. Looked at one way, the industry seems as if it’s booming. Viewed from a different perspective, it looks like trouble is on the horizon. The truth is likely somewhere in the middle of those two extremes. Welcome to the new normal.

Last fall, when speaking at an American Trucking Associations (ATA) economic briefing, ACT Research president Kenneth Vieth described this economic period we’re currently in—this post Great Recession, post recovery upswing—as “the Great Okay” and it’s a description that seems like it will continue to apply for the next year or so.

As to what that actually means in real terms, it seems there is no over-arching trend or mood, except maybe for a cautious attitude to doing business. To illustrate the one-toe-in-the-water approach, let’s look at some the results of Fleet Executive’s Annual Equipment Buying Trends Survey.

This year, 180 fleet managers and owners answered a comprehensive list of questions about their buying preferences, including their purchasing intentions. Answers were provided by executives responsible for all sizes of fleets—from small to large.

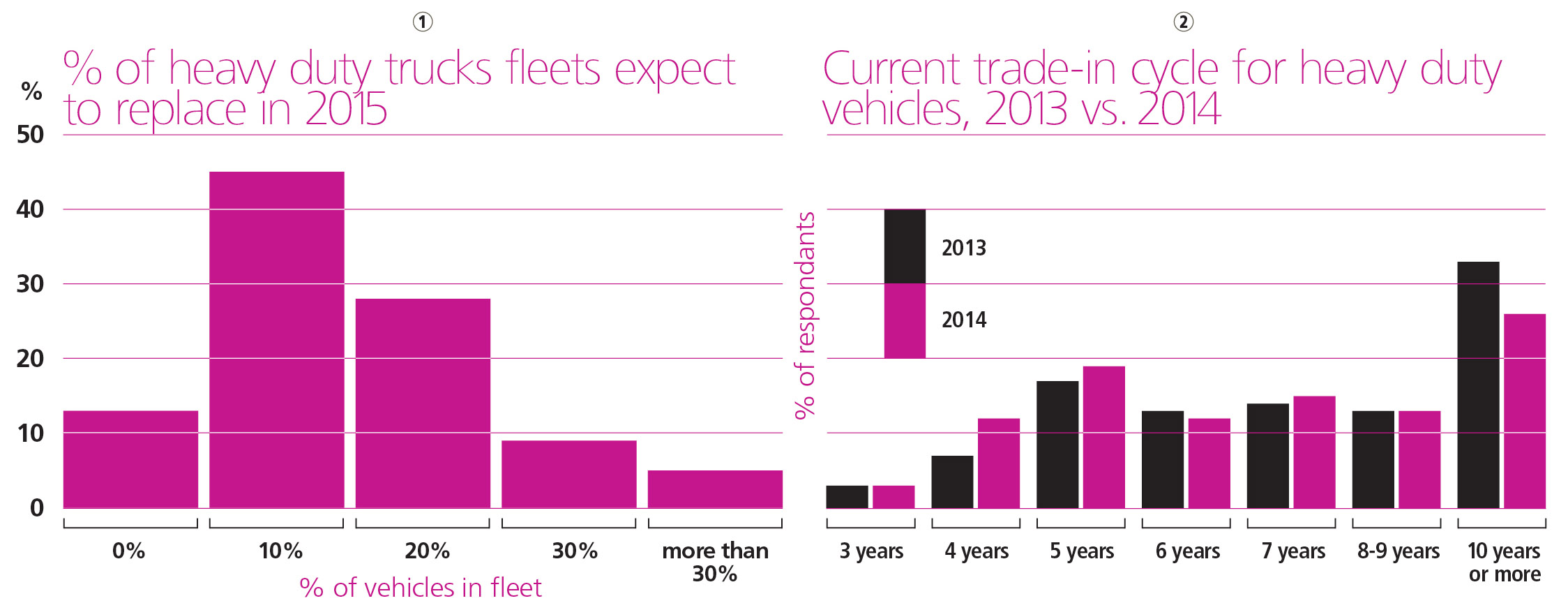

Last year, during the 2013 survey, when asked if they had any intentions of purchasing new heavy duty trucks in 2014, nearly half of respondents (46.8%) said they expected to replace 10% of their fleets; 21.7% said they had no intentions of replacing any trucks, and 20.4% thought they’d swap out 20% of their Class 8 vehicles.

In comparison, when asked the same forward-looking question (“What percentage of your heavy duty fleet do you anticipate replacing next year?”) in the 2014 survey, the results showed some differences. The number who answered zero took a sharp decline, with 13.2% of respondents saying they weren’t planning any replacements. A very similar percentage—45.4%—indicated they expected to update 10% of their trucks, while 27.6% said they’d replace 20%.

If the 10% and 20% replacement categories are combined and viewed as a measure of optimism about the economic outlook of the industry, we see 73% of 2014’s respondents expect they’ll be in the financial position to justifiy at least some major equipment purchases—compared with 67.2% who felt the same way last year—even if they aren’t going on major buying sprees.

Those replacement figures (see graph 1) are pretty much in line with what Kam Hon, managing director of industrials for the Toronto-based rating agency DBRS Ltd. expects.

“The forecast for 2014 compared with 2013 is just about flat. Some people say it’s down a little bit. Some say it’s higher. Our internal expectation is it’s more or less flat. 2015, I would say is just about the same,” he said.

“At the end of the day, it’s just about the economic growth of the continent. We’re still a little bit concerned about the strength of the US economic growth, so we don’t see much impact at this stage of the economy kicking up into a higher gear. We feel the majority of the truck replacement purchasing is over. The big wave has gone. It will just be pretty flat for the next couple of years: we’re talking [total US sales of] 200,000 to 230,000 units. That’s what most people are predicting for 2014. And the same range for 2015. Tack on 10% for Canada, and we’re in that 210,000 to 240,000 range.”

Hon’s concern about the North American economy is fairly easy to discern. Starting in the US, a number of the key economic indicators are mixed at best. During the first quarter of the year non-farm labour productivity decreased 3.2% while hours increased 2.2% and output decreased by 1.1%. The Consumers Price Index increased 0.3% in June, and 2.1% over the last 12 months, driven mainly by a 3.3% rise in the gasoline index. The one positive set of numbers was the June unemployment rate, which declined to 6.1%. Overall, the US unemployment rate dropped 1.4% over the first half of 2014.

In contrast, the unemployment rate in Canada actually rose—albeit slightly in June—0.1 percentage points to 7.1%. Although, there were more people working in June 2014 than June 2013, it was just a fractional amount higher: 0.4%. According to Statistics Canada, that tiny increase represents “the lowest year-over-year growth rate since February 2010, when year-over-year employment growth resumed following the 2008-2009 labour market downturn.” The June job figures also showed job losses for all age groups except people 55 years of age or older.

Other Canadian economic indicators look equally weak. The country’s real gross domestic product grew 0.1% in both March and April, but the output of goods-producing industries fell 0.3% in April.

One bright spot was the RBC Canadian Manufacturing Purchasing Managers’ Index, which registered a six-month high of 53.5 in June.

“The latest RBC PMI data indicates that in June, Canada’s manufacturers experienced the best conditions for growth in half a year,” said Craig Wright, senior vice-president and chief economist, RBC. “We expect that those conditions will further improve going forward supported by a strengthening global economy, increases in external demand for domestic goods and a depreciating Canadian dollar.”

Moving away from the general economy and focusing on the trucking industry itself, the numbers and statistics are a mixed bag at best. ACT Research reports that in June, North American Class 8 truck sales were up 28% versus June 2013, with a total of 26,729 orders placed. In contrast, however, Classes 5-7 net orders fell for the second straight month, coming in at 15,055 units.

The most recent ATA tonnage index report finds the June index dropped 0.8% to 128.6. Compared with June 2013, the seasonally adjusted index increased 2.3%, down from May’s 3.3% year-over-year gain. According to the ATA, this year-over-year increase was the second smallest in 2014, following a 1% gain in January. Additionally, that 128.6 figure is down 1.9% from the all-time high of 131 recorded in November 2013. So that looks bad, but the question is how bad? Yes, the numbers slipped in June, but they’re just fractionally off, and in the grand scheme of things, they aren’t that far away from the record high.

When compared to the first half of 2013, the first six months of 2014 showed an increase of 42% in spot market freight volumes according to the data compiled by TransCore Link Logistics’ Canadian Freight Index. Despite setting six consecutive monthly volume records, the index also shows that from May to June, load volumes were flat, and that second quarter volumes dropped 4% versus Q1 2014.

Our own Transportation Buying Trends Survey found 58% of Canadian shippers expect to move higher volumes of goods this year compared with 2013, with 45.3% of respondents saying they expect the increase to be between 5% and 10%. That same survey found that most shippers expect to increase their use of both LTL and TL services by 39% and 30% respectively.

When asked about how optimistic they feel, carriers answering the same survey ranked their positive outlook level at 6.1 on a scale of 1 to 10. And 40% said they expected to see an increase in volume. Looking deeper into that figure, it seems there are different feelings expressed by different sized carriers. Large carriers rank their optimism at 6.75. Medium carriers place theirs at 6.38, but small carriers come in lower than the average. They peg their number at 5.55.

In spite of the hodgepodge of conflicting data, generally the mood about the near future of the industry seems positive.

In an RBC Capital Markets Equity Research Report, RBC Dominion Securities Inc. analyst Walter Spracklin explained why the bank is upbeat about trucking.

“We are raising our estimates for the Canadian trucking companies in our coverage space on evidence we have uncovered that points to improving industry fundamentals, strengthening our earnings expectations for 2015 and beyond. Our optimistic outlook reflects positive indications provided in recent discussions with senior executives of private trucking companies regarding the three pillars of profitability for this industry: volume, capacity, and price. Put simply, we believe the industry is approaching an inflection point where demand (via higher volumes) is beginning to overtake supply (through tighter capacity), affording carriers greater pricing power (in the form of higher freight rates) that should translate into improved financial results going forward.”

Dan Goodwill, president of Dan Goodwill and Associates Inc. in Toronto, also feels generally good about the Canadian trucking industry. “I’d say my sense of the overall trucking environment today is probably the best it has been in years. My sense is it’s pretty buoyant right now and that’s a result of several factors. But I think if you talk to truckers, they will tell you demand is better today than it has been in some time.”

Hon too, said he’s “mostly positive” about the health of the industry. “The growth in the economy is what we call a structural growth trend, so truck demand is still up, but it’s in line with the general economic growth of about 3% per year. The trucking industry should still experience a growth trend because we think the North American economy will grow at a modest pace of 2%-3% per year,” he said.

“I expect unit sales to grow on a year-over-year basis. I expect 2014 to be slightly higher than 2013, and 2015 to be similar to 2014. That more or less reflects my sentiments about the US, but I don’t see Canada being any different.”

Note that qualifier “mostly.” Both Hon and Goodwill expressed concerns about issues with the potential to derail the industry. Hon said competition from rail is a threat, since Canadian railways are doing a better job meeting customer demands and improving their service. He mentioned that with the driver shortage, even if companies want to buy new trucks, they can’t get them on the road if they can’t put somebody in the driver’s seat. He also noted the ever-increasing price of diesel.

Goodwill also singled out the driver shortage being problematic, but for slightly different reasons.

“Capacity is a challenge. I think it’s a challenge not because truckers can’t buy trucks, but because of the driver shortage,” he said. “I’ve been reading reports that some trucking companies are actually cutting back on their fleet size because they can’t fill the trucks. That’s a two-edged sword. If there is less capacity, it puts upward pressure on rates, which helps these companies achieve higher yields on their businesses. But on the other side, it means it will be a tougher environment for shippers to get the capacity they need as the years go by.

“There is no simple formula to fix that because shippers don’t want to pay more for freight. An easy solution is for truckers to throw more money at the drivers, pay them more and raise rates. That’s a vicious circle the buying public doesn’t want, but ultimately that’s one of the things that has to happen.”

Financing equipment purchases

Traditionally there were two ways of paying for new trucks. Using cash on hand or asking the neighbourhood banker for a loan. In today’s economy, trucking companies are turning to other sources for financing. Kam Hon of DBRS Ltd., a bond rating agency, said many trucking companies with good credit ratings are looking to insurance companies and pension funds to supply the cash for truck purchases.

“Because of the low interest rate environment right now, they are more than happy to loan it out to get a higher rate of return because money sitting in the bank doesn’t give you any return at all.”

As for the lease versus buying decision, Hon said interest rates and credit ratings are the primary driving factors in the decision making process. He explained if companies can borrow at a rate that is “more advantageous” than the leasing rate, that’s what they’ll do, calling it a very “mechanical decision.” If not, then they’ll lease.

Multiple perspectives

Talking about the Canadian fleet is an easy piece of linguistic shorthand. The trouble is it really doesn’t exist.

Instead of a homogenous, uniform fleet, there are at least three different fleets and they’re based on size: large, medium and small. And if there is one absolute truth that comes out of the 2014 Equipment Buying Trends Survey, it’s that fleets of different sizes seem to have distinct perspectives about almost everything.

When figures are pulled that represent all fleets, the question about whether a company intends to purchase Class 8 trucks next year and if so how many, returned results that included 13.2% of people saying they had no intentions to buy any trucks, 45.4% saying they would replace 10% of their fleets, and 27.6% reporting they would renew 20% of their fleets.

There are almost entirely different responses, however, when the questions are sorted by fleet size. Of those responsible for large fleets, only 4.9% said they wouldn’t replace any trucks. In contrast, 12.5% of medium fleet executives and 22.2% of small fleet executives said they won’t replace any vehicles. The 10% replacement level earned responses from 31.7% of large fleets, 56.3% of medium fleets and 33.3% of small fleets. At 20%, the results were as follows: 41.5% of large fleets, 21.3% of medium fleets and 27.8% of small fleets expect to replace this many trucks in 2015.

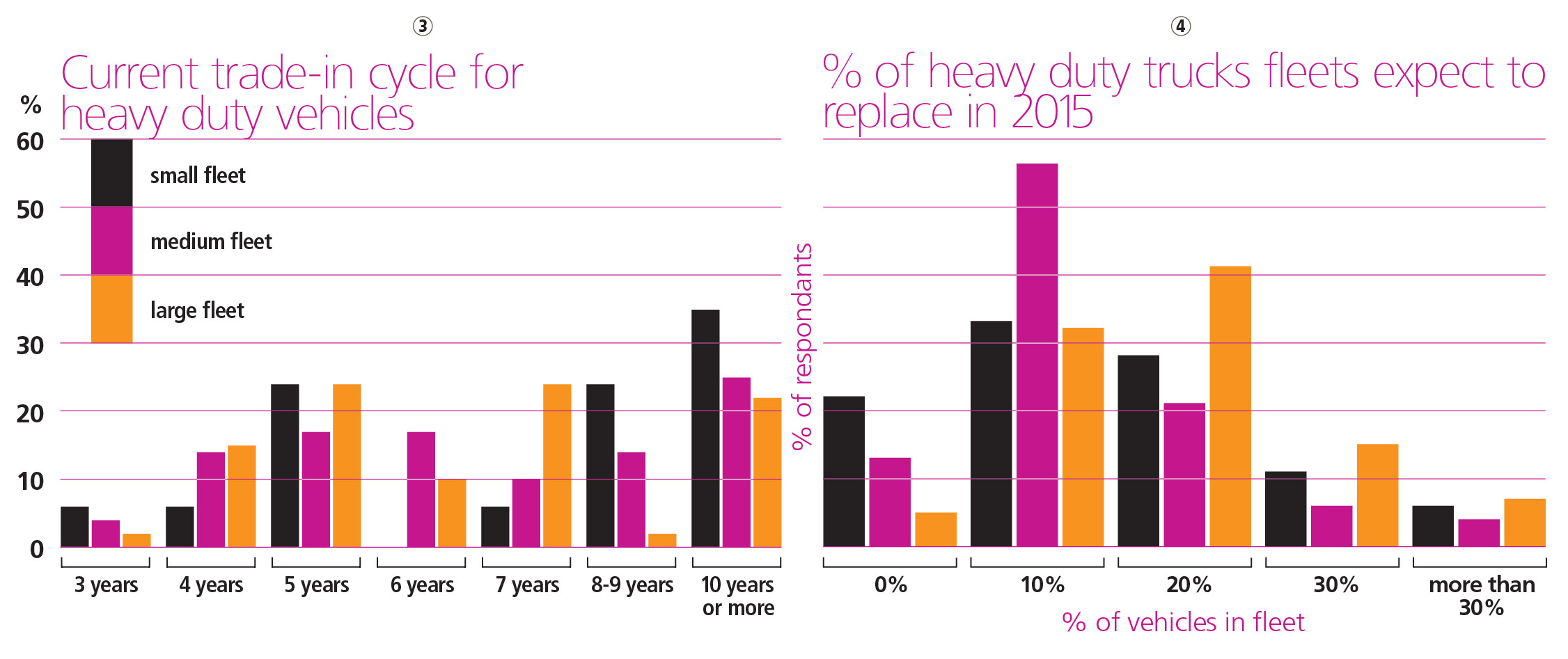

Trade in-cycles for heavy duty vehicles varied wildly depending on fleet size. (See graph 3 below.)

Compared with small and medium fleets, large fleets have purchased a considerably lower percentage of used trucks, with 55.0% responding in the affirmative that they have bought previously owned vehicles. For medium sized fleets, the response was 71.4% and for small fleets it was 76.5%. Looking forward to 2015, 17.1% of large fleets thought they would purchase a used truck next year, as did 16.7% of medium fleets and 35.3% of small fleets.

Different sized fleets also seem to have distinctive preferences when it comes to equipment choices. For example, large fleets select automatic transmissions as their number one choice, whereas most medium fleets indicate they prefer a 13-speed manual, while small fleets rank 18-speed manuals as their preferred gearboxes.

Dan Goodwill of Goodwill and Associates, offered some perspective about why smaller fleets made some of the choices they did, particularly when it comes to relying upon older, simpler trucks.

“My overall feeling is that smaller companies are having a tougher time than larger companies. I think there is going to continue to be consolidation,” he says.

“There is so much pressure on small companies now. You can’t hire drivers, so with a small fleet, you can’t be as flexible and have the capacity a larger fleet has, and with all of the restrictions in the US and in Canada too, to some extent—hours of service and other regulatory issues—it’s just really hard for a small trucking company unless you’ve got a very good niche and you have differentiated yourself in the niche you are in. But if you’re a me-too trucking company, a small one, trying to compete with bigger guys who have better technology and more flexibility, the you are in tough. I think some of them are just not going to be able to hang on in there.”

Have your say

This is a moderated forum. Comments will no longer be published unless they are accompanied by a first and last name and a verifiable email address. (Today's Trucking will not publish or share the email address.) Profane language and content deemed to be libelous, racist, or threatening in nature will not be published under any circumstances.