ECONOMIC TRUCKING TRENDS: Spot market rates, Class 8 truck demand and trucking conditions all continue to strengthen

Trucking data crossing our desks over the past week show continued improvements in spot market rates, as freight demand outpaces capacity additions.

Fleets are getting their orders in for trucks ahead of costs related to EPA27 emissions regulations that take effect in January.

And spot market rates continue to improve, especially if you’re in the flatdeck sector. Let’s have a look:

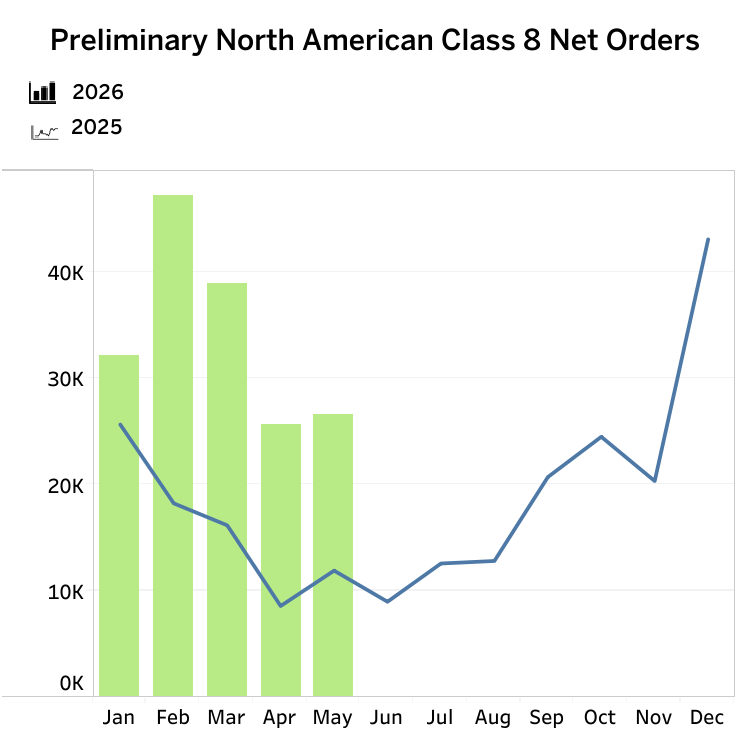

Strong Class 8 orders point to improving freight outlook

North American fleets continued to place truck orders at a robust pace in May, with both ACT Research and FTR reporting Class 8 demand remained well above historical norms despite limited remaining 2026 production capacity.

ACT Research pegged preliminary Class 8 net orders at 26,500 units in May, up 12% from April and 103% year over year. Meanwhile, FTR reported preliminary Class 8 orders of 26,600 units, up 4% month over month and 124% higher than the same period last year.

“Despite the lack of build slots remaining in 2026 and entering what is historically a weak seasonal order period, new equipment demand remains buoyed by materially improved spot and contract rates, on top of regulatory clarity,” said Carter Vieth, research analyst at ACT Research.

FTR senior analyst Dan Moyer pointed to many of the same factors, citing replacement demand, improving freight rates, rising utilization, tighter capacity and some EPA27 pre-buy activity as drivers of order strength.

Both firms suggested truck makers could see remaining 2026 production slots effectively sell out earlier than normal. Through May, FTR said Class 8 orders were running 112% ahead of last year’s pace and 28% above the current order cycle’s year-ago level.

The strong demand wasn’t limited to heavy-duty trucks. ACT reported preliminary Classes 5-7 orders reached 19,000 units in May, up 32% year over year. Vieth said the increase may reflect both economic resilience and some dealer stocking ahead of EPA 2027 emissions regulations.

While order activity remains strong, both analysts cautioned that risks remain. FTR noted softer retail sales, uneven carrier profitability, financing pressures and geopolitical uncertainty could still temper demand later in the year.

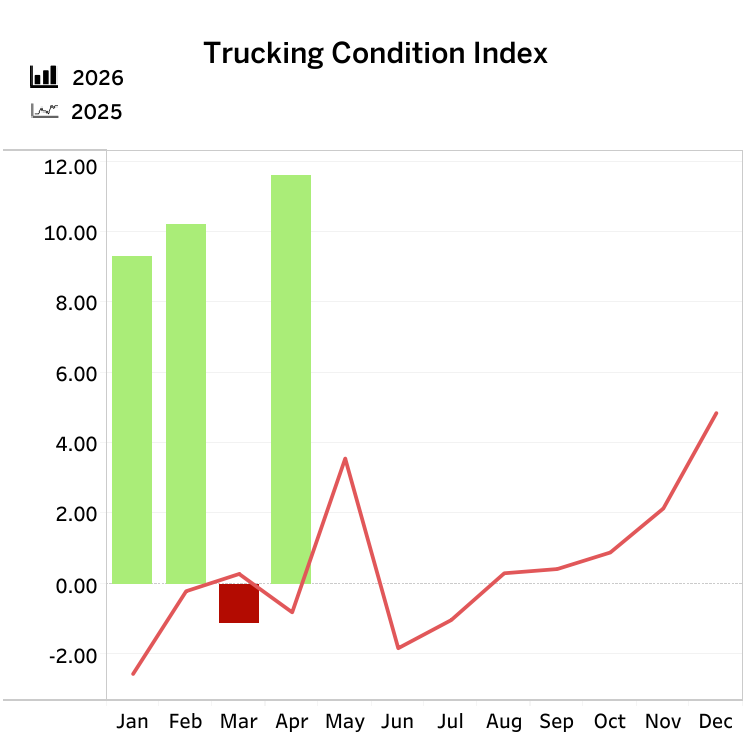

Trucking conditions drastically improved in April

Carrier conditions improved dramatically in April, with FTR’s Trucking Conditions Index (TCI) surging to 11.6 — its strongest reading since February 2022.

The jump from March’s negative 1.1 reading was driven primarily by stronger freight rates and higher capacity utilization, which more than offset the impact of elevated fuel costs.

“While surging fuel costs in the past couple of months obviously created cash flow crunches for many operations, tight capacity and surging freight rates are more than offsetting that challenge,” said Avery Vise, FTR’s vice president of trucking.

Vise noted freight volumes continue to grow, though not as quickly as rates. He highlighted flatbed trucking as a particularly strong segment, benefiting from both constrained capacity and increased demand tied to data center construction and a modest recovery in manufacturing activity.

FTR expects trucking conditions to peak this summer but forecasts a favorable operating environment for carriers through its two-year outlook. The TCI measures freight volumes, rates, capacity, fuel prices and financing costs, with double-digit readings indicating significant positive market conditions.

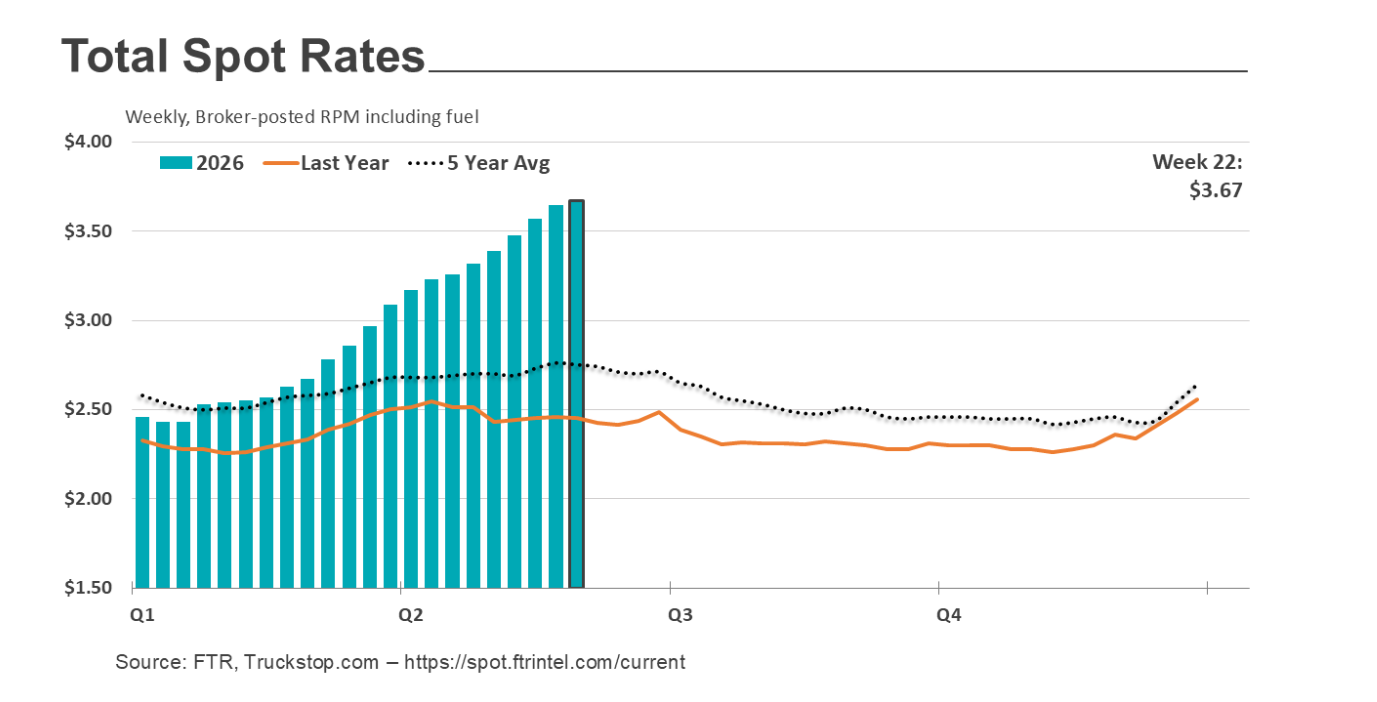

Spot market continues tear

The spot market continued its remarkable run during the week ending June 5, with rates reaching new highs and capacity remaining significantly tighter than a year ago.

According to Truckstop.com and FTR Transportation Intelligence, all four key market indicators increased during the week. The Market Demand Index (MDI) climbed 8.2 points to 208.9 as load postings rose 9.4% and truck postings increased 5.1%. Despite the increase in available trucks, demand continued to outpace capacity, keeping the market exceptionally tight.

Compared to the same week last year, the MDI was up 115.5 points, or 123.7%, highlighting the dramatic shift in spot market conditions.

Broker-posted spot rates rose 0.7% week over week to a record $3.67 per mile, while national diesel prices fell 17 cents to $5.33 per gallon.

Flatbed freight remained the market’s strongest segment. Flatbed spot rates increased for the 28th time in the past 29 weeks and established another all-time high. Truckstop and FTR attributed the sustained strength to ongoing data center construction activity, an emerging recovery in manufacturing and persistently tight flatbed capacity.

The outlook for flatbed demand remains favorable.

“With the ongoing push to build data centers and the early-stage recovery in the manufacturing sector, coupled with tight flatbed capacity, Truckstop and FTR see little reason to expect any substantial softening soon,” the companies said.

Dry van and refrigerated freight showed more typical seasonal patterns. Dry van spot rates edged lower after coming within three cents of an all-time high the previous week, while refrigerated rates also declined modestly. However, both segments remain exceptionally strong compared to year-ago levels.

Spot rates for van equipment are still running more than 50% higher than during the same period in 2025, even after recent pullbacks. Fuel-adjusted dry van and refrigerated rates remain nearly as strong on a year-over-year basis as all-in rates, suggesting underlying freight fundamentals continue to support pricing.

Have your say

This is a moderated forum. Comments will no longer be published unless they are accompanied by a first and last name and a verifiable email address. (Today's Trucking will not publish or share the email address.) Profane language and content deemed to be libelous, racist, or threatening in nature will not be published under any circumstances.

-

Why do people hide behind fake names when they post criticisms? US data is more readily available (Loadlink doesn’t share rate trends) and many of our readers operate in the United States. We also have many readers from the U.S. — more than half, in fact.

-

Why do you assume it’s a fake name? Does Trucknews now require proof of identity before posting opinions, rebuttals, and/or criticisms?

You answered a criticism by questioning the name on it. Nice deflection. That’s not a rebuttal. So let me put the point back where it belongs: nobody disputes that more than half your readers are American, or that U.S. data is easier to pull. The complaint was never that you cited U.S. sources. It’s that you ran a piece on strengthening freight conditions and let U.S. numbers stand in for a Canadian market that doesn’t move the same way — without one line questioning whether the two track together. Right now they don’t. The U.S. economy is firing while Canada just slipped into a technical recession, so American conditions can’t be read as a stand-in for the Canadian market.

“Easier to source” isn’t “applicable.” That’s an editorial judgement, and it’s the one I’d expect Trucknews, of all outlets, to make.

And on rate trends — sure, LoadLink keeps theirs behind a paywall. Which means the Canadian numbers exist; someone just has to invest in them. Reaching for free U.S. data instead is a choice, not a necessity. That’s the whole complaint in one line: the market you actually serve is harder to cover, so it gets covered through someone else’s lens. I’d have thought that’s exactly the gap a Canadian trade publication exists to close.

-

Why are you quoting U.S. research numbers. None of the sources in your article give any consideration to the Canadian spot market when researching their numbers. Is Trucknews incapable of doing its own research, or is it just comfortable copying whatever is published in CCJ and calling it a day?

Of course the U.S. freight market is robust. The entire U.S. economy is robust. Any kid that can add 2+2 knows that.

There’s no strengthening of spot market rates in Canada. How could there possibly be? The Canadian economy is, for all intents and purposes, dead. How do you get a thriving freight industry out of a dead economy?

Did any of the editorial staff even look at, or question, this article before publishing it?

Come on Trucknews … do better !!!